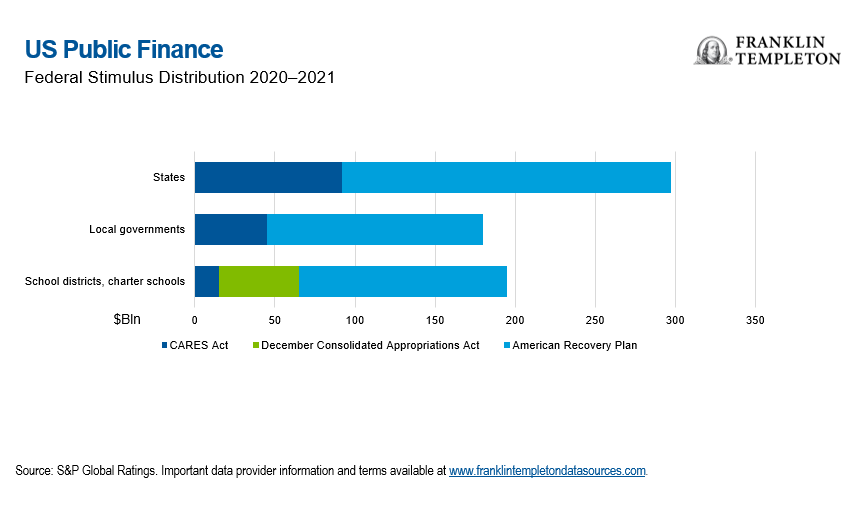

The recent passage of US President Joe Biden’s $1.9 trillion COVID-19 relief package, “The American Rescue Plan Act of 2021,” not only includes checks for individuals, but also allocates funds for state and local governments, so it should provide a boost to states, cities and counties reeling from the pandemic. While the CARES Act and the last round of stimulus in December restricted funding to coronavirus-related efforts, this time around, local governments can use federal dollars for more flexible purposes. States want revenue replacement aid—aid which can be used for any purpose to replace lost revenues—and they got it. Aid will be received in two pieces and can be used through 2024.

We caution that this sort of blank spending check comes with a potential moral hazard, so good governance at the state and local level will be paramount in terms of allocating these funds judiciously, in our view. How this process plays out will need to be watched very closely as it can have an impact on the credit outlook for the municipality both in the short- and long-term time periods.

Closing Budget Gaps

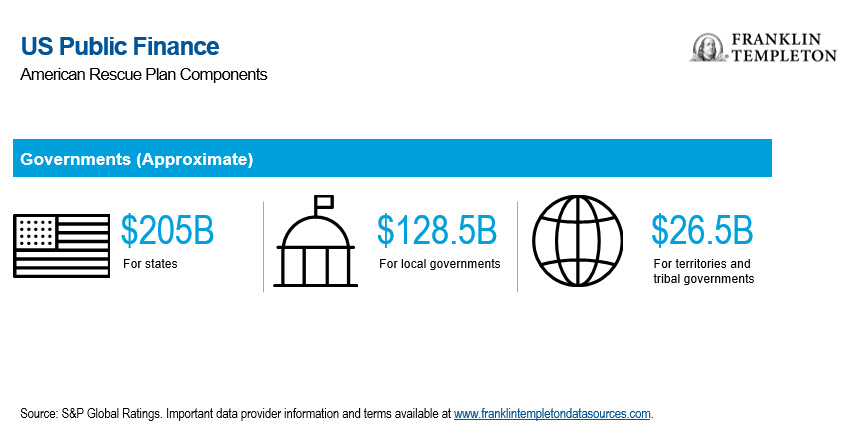

Taxes represent the primary source of revenue for state and local governments, and that revenue stream dramatically declined amid pandemic shelter-in-place policies. The new relief package allots $195.3 billion for states, territories and tribal governments, and $130.2 billion for cities and counties. The legislation attempts to equitably divide up the money, with funds allocated using a variety of formulas, but $25.5 billion will be equally divided among states, so no state will receive less than $500 million. The remainder is allocated based on the percentage of seasonally adjusted unemployment from October-December 2020. Local governments will receive $45.6 billion, based on a formula incorporating population, growth, poverty rates and housing density; states will have $19.5 billion to distribute to “locals” and $65.1 billion will go to counties based on population.

In addition, money is also available for specific areas like transit, education and even $10 billion for capital projects, including broadband expansion.

Currently, it’s budget season for these entities, so the aid comes at the perfect time. State and local governments can craft their budgets for the upcoming fiscal year (FY) knowing how much aid they will receive. At this same time last year, budgets were assembled based on significant unknowns. However, deciding how to use the funds is still a political decision, with conflicting interests looking for a piece of the pie.

This stimulus aid is a one-time infusion of money, so we think it would be most prudent for issuers to spend funds they receive for one-time uses. If the funds are used for recurring programs, then governments would have to find new funding sources for those programs going forward, which could be problematic, particularly for poorly managed entities.

Many state and local governments introduced their FY2021 and FY2022 budgets with no assumptions of additional federal aid, which we view as good budgeting technique since the money wasn’t guaranteed at the time. While government revenue has generally been outperforming early estimates during this pandemic period, many governments are still contending with budget deficits for FY2022. This aid package plus the package received in December could help close if not eliminate those budget gaps.

The aid will be positive for everyone, but states and locals which can use the money for revenue replacement should benefit most. Although schools have benefited in prior rounds of stimulus, this allocation is significantly larger than the previous ones. Given concerns over learning loss and safely reopening schools nationwide for in-person education, this aid will be very helpful.

Since the stimulus was passed, we’ve already seen two ratings agencies upgrades of the state and local government sector outlook to stable from negative, we’ve seen one of the weakest school districts upgraded, and we have seen outlooks generally improve. Many observers predict that there will be more upgrades than downgrades this year. We are still waiting for some additional direction from the US Treasury regarding eligible uses for the aid, but even if there are some restrictions, we expect it to be an overall positive.

The (Solid) Shape of States

As we outlined in our recent paper, “COVID-19 Disrupts Municipalities,” states overall were at all-time credit strength heading into the pandemic. Coming out of a 10-year period of economic expansion after the global financial crisis, reserves were rebuilt and most governors were recommending new spending programs. They were in good shape for a shock, with many tools in their financial toolbelts to deal with the pandemic. As such, the catastrophic-looking economic downturn didn’t injure state and local governments as badly as it could have.

Most states have progressive income tax structures where the wealthy pay more than the poor. The increase in unemployment from the pandemic was felt primarily among low-wage earners, not the wealthier individuals who pay a significant portion of income taxes. So, the income tax stream wasn’t severely curtailed. Capital gains represent a significant portion of income tax revenues as well, and given the stock market ended the year near all-time highs, that component also remained healthy.

As of 2020, every state but Vermont had a balanced budget requirement, so while details vary, states cannot spend more than they collect in revenue. When shortfalls emerge, states have to determine how to close the gap through spending cuts, drawing upon reserves, or other measures.

Given stimulus is on the way just in time for the new budget season, it should help governors reduce or even eliminate budget gaps and avoid making unpopular spending cuts.

Muni Market Matters

As investors, we are keenly watching how state and local governments use the new stimulus funds. Productive uses could include economic development, capital spending, and support of COVID-19 vaccine distribution and relief programs. We could also see governments use it to bring furloughed workers back, reduce outstanding payables or other purposes that make good budget sense. We are also hearing quite a bit of talk about using it for infrastructure, in addition to what could be made available in a future federal infrastructure bill.

In the California city of Fresno, for example, Mayor Jerry Dyer faced a $25 million budget deficit, and was considering layoffs of approximately 200 city employees, including police and firefighters—now apparently off the table.1

In Ohio, the city of Cleveland used its reserves to avoid layoffs over the past year, in addition to reducing staff through attrition. While we don’t have details yet on exactly how the new funds will be allocated, Mayor Frank Jackson’s new budget proposes spending $659.3 million on general operations (up from $651.2 million last year) and Ohio governor Mike Dewine was quoted as focusing on upgrading infrastructure—particularly broadband throughout the state.2

Seattle Mayor Jenny Durkan stated she would be proposing a plan to support downtown and neighborhood small businesses, and address the critical needs of residents, including those facing homelessness.3

In Erie County, New York, plans to lay cable to expand internet service were canceled when COVID-19 ravaged the county’s budget, but one official there stated it would likely be revived with the $178 million the county will receive.4 An official in the tiny town of Coventry, Connecticut, said its fund allotment might be directed toward improved ventilation in schools, recreational programs and temporary staffing for ambulances.5

In our view, unproductive uses of the relief funding would include starting new spending programs that will continue and require funding in future fiscal years, after the funding dries up. That type of activity could exacerbate future budget challenges or even create budget challenges when there otherwise wouldn’t have been. We would note that states that were weak going into the pandemic are still likely to be weak coming out, regardless of the cash infusion. The stimulus will certainly help some weak issuers, but we will be watching carefully to make sure that the weaker actors don’t squander it and don’t put off making decisions to bring budgets closer to a structural balance.

Even with certain states doing well—California, for example, announced an unexpected $15 billion surplus—good governance going forward is vital, and something we pay close attention to as investors. No doubt, there will be some bad spending decisions, which is why we think an active approach to investing in the space is warranted. To us as investors, it is all about understanding the full risk of the credit and aligning that with relative value, while avoiding the really troubled situations.

Inflation and Interest Rates: Mind the Curve

How this stimulus will impact the municipal bond market is an important question. Muni bonds are issued to finance projects at the state and local levels, and the idea is to amortize that debt over the average useful life of whatever asset is being financed, which spreads the cost over taxpayers that are benefiting from the project. Serial maturities can be very attractive for investors looking for shorter duration fixed income securities. But given all the stimulus in the economy, rising inflation and interest rates has come up as a concern.

Of course, municipal bonds are fixed income instruments, and will generally react to fundamentals similarly to other fixed income instruments. Munis do typically react to interest rate changes (whether tied to inflation or other factors) but have tended to react with a little lower volatility than the Treasury market. Treasuries are sort of a “perfect” credit quality-type of security and so they tend to only react to interest rate changes because in essence, there’s no real credit risk with Treasuries. Even though munis tend to have very high credit quality as an asset class overall, they do exhibit more credit risk than Treasuries. That additional credit risk becomes part of the valuation and pricing equation and can tend to dampen the impact of interest-rate changes. For this reason, munis can tend to have less volatility to pure interest-rate changes than Treasuries.

Price volatility is related to two main factors: duration and credit quality. Duration is the tool that we use in fixed income to measure interest rate volatility. The longer the duration of the bond, the more volatility it will have in response to interest rate changes. Then there’s credit risk or spread. We think of this as whether a credit security is on the upswing or on the downswing—is a credit upgrade likely, or downgrade?

Just like the muni-to-Treasury relationship is very dynamic, different yields of different states around the country are also dynamic. A lot of it depends on the technical features of each state, including whether there is more supply coming in a particular state, or if there’s a credit fundamental issue in a particular state versus another. But today, we are finding opportunity within nearly every sector, as most have come through the pandemic fairly well and some weren’t impacted much—utilities, for example.

From a regional investment perspective, we are cautious about communities with tourism-driven economies, as there’s still uncertainty about travel, which may not fully rebound for several years.

But today, as we address the pandemic, we’ve spent a lot of time trying to leverage data and be more responsive as investors, especially when interesting opportunities appear in the market.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Because municipal bonds are sensitive to interest rate movements, a municipal bond portfolio’s yield and value will fluctuate with market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the portfolio’s value may decline. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value.

Any companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

___________________________

1. Source: New York Times, “Stimulus Bill Transforms Options For State and Local Governments,” March 15, 2021.

2. Source: Cleveland.com, “Cleveland, Ohio governments to get big money as part of new federal stimulus plan. How will they spend it?” March 12, 2021.

3. Source: The Seattle Times, “Washington state to get billions of dollars for schools, transit and cities as COVID-19 relief bill clears Congress,” March 10, 2021.

4. Source: New York Times, “Stimulus Bill Transforms Options For State and Local Governments,” March 15, 2021.

5. Source: Hartford Courant, “Federal stimulus bill will bring billions to Connecticut cities and towns. Here is what to know,” March 11, 2021.