Q3 2021 Outlook: Summary

With society and economies in transition, investors must underwrite to a wide range of potential outcomes. Progress on vaccinations, central banks beginning a cycle of tightening policy, and earnings growth are important variables that are difficult to gauge. Given the uncertainty embedded in the underlying core markets, we believe it is prudent to focus hedge fund investments on alpha generating non-directional strategies.

Strategy Highlights

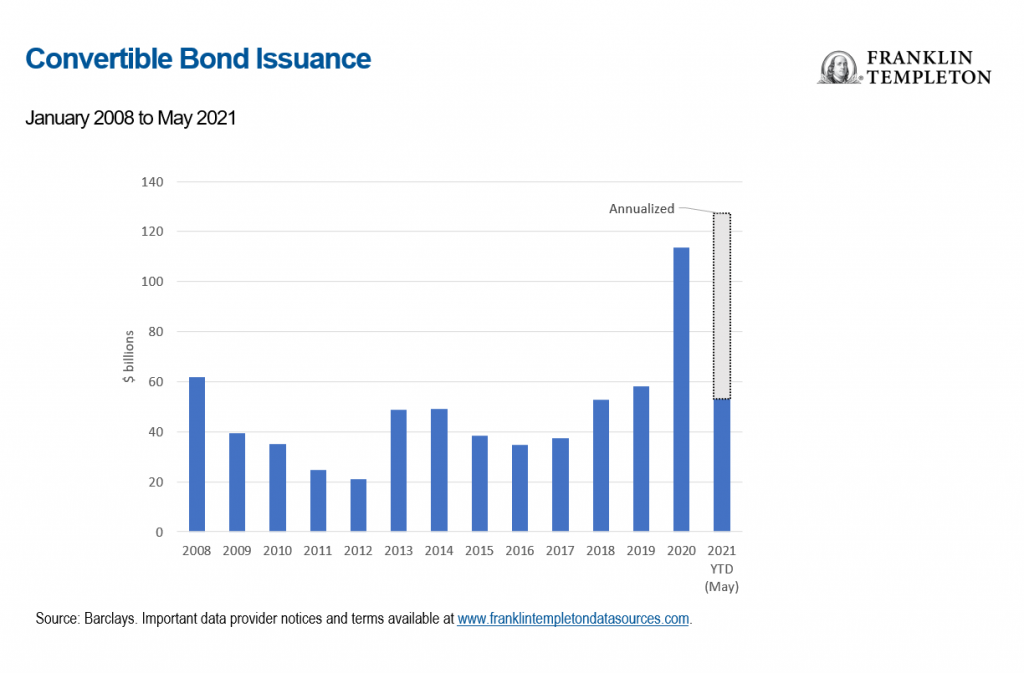

- Relative Value: A robust primary market represents a tailwind for convertible bond managers. More bonds to underwrite, improved liquidity and trading opportunities, and the ability to flip bonds into the secondary market are among the positives.

- Global Macro: Managers focused on macro factors may benefit from a rich opportunity set as data releases and policy paths continue to play a critical role across markets.

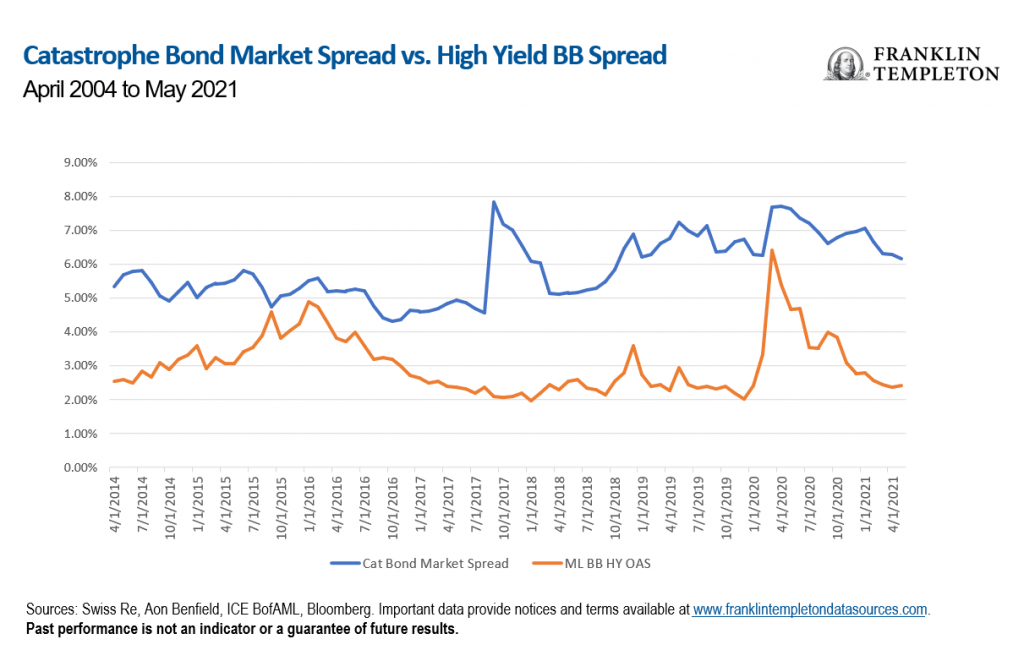

- Insurance Linked Securities (ILS): Flows into the market brought on a very active second-quarter (Q2) new issuance period. While spreads have tightened, they remain attractive versus corporate high yield entering the key summer ILS risk period.

[perfectpullquote align=”full” bordertop=”false” cite=”” link=”” color=”” class=”” size=”11″]

Strategy |

Outlook |

| Long/Short Equity | Active, long-duration, fundamental long/short equity managers may be challenged by the market’s volatile rotations. Investors are focused on macro, and companies are navigating toward “back to normal” while their stocks simultaneously trade at high valuations. |

| Relative Value | Favorable outlook for convertible and volatility arbitrage given continued strong issuance and inefficient pricing. Outlook for fixed income arbitrage is more muted due to central banks’ success in depressing global rate volatility. |

| Event Driven | Expect continued active supply of corporate events due to ample liquidity, peak valuations, and continued management team incentives to grow market share and earnings. |

| Credit | Spreads remain near historic tights, which favors trading-oriented strategies such as long/short credit at the expense of more directional ones such as distressed and direct lending. Pricing in structured credit remains inefficient, and managers expect dispersion to persist in certain sectors. |

| Global Macro | Macro developments continue to drive global markets with managers focused on these factors facing a potentially rich opportunity set over the medium term. Shifting market narratives around future policy paths may favor nimble and opportunistic trading styles. |

| Commodities | Tighter supply and demand will likely lead to more relative value trading opportunities. We are encouraged by the discipline of many long/short commodity managers as they are tightly managing capacity. |

| ILS | June 1 renewals continued the trend of higher reinsurance pricing over a multi-year period. While spreads have tightened, they remain attractive versus corporate high yield entering the key summer ILS risk period. As Q3 is peak hurricane season, its outcome will have an influence on forward pricing. |

[/perfectpullquote]

Macro Themes We Are Discussing

As we reach halftime of the calendar year, investors go into the locker room with some knowledge of the pandemic recovery and some new concerns to monitor in the second half of 2021 and into 2022. The world is likely not returning to the same as before and there will likely be companies and countries better positioned for the new environment than others. The speed of recovery may vary among regions due to disparate global vaccine distribution leading to potentially divergent central bank policies. The underlying fuel of market valuations, investor preferences, and relative valuations is liquidity (central bank issuance). Key questions to watch are when will these accommodative measures be reduced and how will investors react?

Going forward the environment for active management looks very rich. Hedge funds are the ultimate expression of active management with the ability to invest from both the long and short side of securities as well as tactically adjust gross exposure.

Is inflation transitory or a big problem brewing?

Our base case is inflation is transitory; however, we are watching the data very closely in acknowledgement the tail scenario is possible, and any upside surprises would have a large impact on markets. We expect supply chains and pent-up excess demand due to COVID-19 to normalize in the second half of 2021 into early 2022. Commodity managers had a good start to the year, on both directional and relative value risk taking. We expect emerging markets to benefit from delayed reopenings and normalization of global trade. Global macro managers were mostly loaded up on the “reflation trade” early in the year, but then as the trade gets crowded and inflation expectations became subdued, there was a rollover in positioning by the end of Q2 2021.

Will tax resolution be bullish or will increased taxes reprice the market?

Taxes are front-and-center topics at both the corporate and personal levels. The G7 have reached a historic deal backing a global minimum corporate tax rate with technology companies and tax havens potential targets of this deal. Domestically in the United States, personal tax rates and vehicles are under increased scrutiny with changes expected in the second half of 2021. Globally, there is a trend of wealth re-distribution toward the less fortunate.

How much good news is left? Is good news already priced into the market?

Actual earnings and associated guidance are both expected to be very strong in the second half of this year. Economic surprises have been to the upside, employment is trending higher, housing is very strong, and central bankers have been very accommodative. That said, we find ourselves asking “how much good news is left?” Recent Federal Reserve (Fed) comments suggesting a stance of less dovishness rattled the markets for a few days. Central banks are walking a tight rope of being accommodative to keep the economic engine running and avoiding a scenario of either sustained inflation or deflation. They have been over-communicative in preferring to have the economy run hot as opposed to run cold.

Generally, all news has been good for now, but market sentiment can change very quickly—and positioning even faster. We see signs of excess liquidity and are on heightened inflation watch, while at the same time monitoring how forward earnings growth estimates might slow and how the end of stimulus checks and debt forbearance policies might impact consumer spending.

In short, the equity, bond, commodity and currency markets may be approaching a fork in the road during the second half of 2021. Nimble hedge fund managers who are able to “turn both ways” may best be able to actively manage through the upcoming fundamental “traffic.”

Strategy Highlights

Relative Value

The convertible bond market has experienced a resurgence of new issuance since the onset of the pandemic. In 2020, issuers flocked to the market to quickly raise rescue deals, and others sought to monetize the volatility in their stock prices. That activity attracted new investors, which in turn created a positive feedback loop. Momentum carried into 2021, and the primary market is on pace to surpass last year’s record issuance. Strong new issuance represents a tailwind for convertible arbitrage strategies for several reasons.

First, a greater number of bonds means an expanded opportunity set. Experts in the space can discern attractive new issues from those that are likely to trade poorly. Second, the positive feedback loop previously mentioned means improved liquidity characteristics and trading opportunities given new market participants. Investors that cross over from high yield, for example, into convertibles may demonstrate different behavior and preferences than dedicated funds, creating a more diverse investor base. Finally, an active primary market represents an opportunity for investors with strong connections to the Street to secure allocations and flip bonds into the secondary market for a profit. As a result, we find the opportunity set in converts to be attractive.

Global Macro

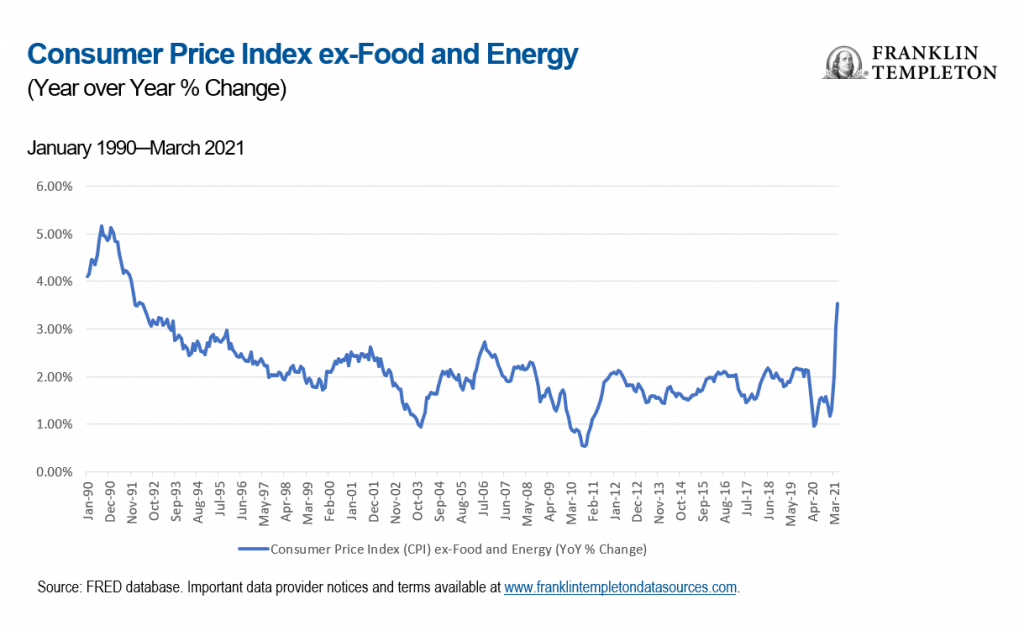

Data continues to show signs of recovery as global economies reopen with the rollout of vaccines and roll back of some restrictive travel and social distancing measures. Surging inflation has taken center stage with recent readings well above the Fed’s stated long-term average target of 2%. As economists and investors debate the persistence of this inflation, markets across asset classes have reacted to a potentially earlier-than-expected shift in central bank policy. Future data releases and policy rhetoric is likely to have a meaningful impact on market prices over the medium term. Managers focused on these factors may be well-placed to find attractive opportunities arising from heightened policy uncertainty or the establishment of market trends.

Inflation Surging as Economies Reopen

Inflation persistence may drive policy measures and asset prices going forward.

Insurance-Linked Securities

Investors favor lower-risk ILS strategies, primarily catastrophe (cat) bonds, which offer the most liquidity. Despite a very active calendar in Q2, we expect a seasonal decline in issuance as we enter US hurricane season. ILS continues to offer attractive relative valuation versus corporate credit. We will closely monitor Q3 event activity, which should provide insight into forward-looking pricing and sub-strategy valuations.

What Are the Risks?

All investments involve risks, including possible loss or principal. Investments in alternative investment strategies and hedge funds (collectively, “Alternative Investments”) are complex and speculative investments, entail significant risk and should not be considered a complete investment program. Financial Derivative instruments are often used in alternative investment strategies and involve costs and can create economic leverage in the fund’s portfolio which may result in significant volatility and cause the fund to participate in losses (as well as gains) in an amount that significantly exceeds the fund’s initial investment. Depending on the product invested in, an investment in Alternative Investments may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. There can be no assurance that the investment strategies employed by K2 or the managers of the investment entities selected by K2 will be successful.

The identification of attractive investment opportunities is difficult and involves a significant degree of uncertainty. Returns generated from Alternative Investments may not adequately compensate investors for the business and financial risks assumed. An investment in Alternative Investments is subject to those market risks common to entities investing in all types of securities, including market volatility. Also, certain trading techniques employed by Alternative Investments, such as leverage and hedging, may increase the adverse impact to which an investment portfolio may be subject.

Depending on the structure of the product invested, Alternative Investments may not be required to provide investors with periodic pricing or valuation and there may be a lack of transparency as to the underlying assets. Investing in Alternative Investments may also involve tax consequences and a prospective investor should consult with a tax advisor before investing. In addition to direct asset-based fees and expenses, certain Alternative Investments such as funds of hedge funds incur additional indirect fees, expenses and asset-based compensation of investment funds in which these Alternative Investments invest.

Important Legal Information

This information contains a general discussion of certain strategies pursued by underlying hedge strategies, which may be allocated across several K2 strategies. This document is intended to be of general interest only and does not constitute legal or tax advice nor is it an offer for shares or invitation to apply for shares of any of the funds employing K2 strategies. Nothing in this document should be construed as investment advice. Specific performance information relating to K2 strategies is available from K2. This presentation should not be reproduced without the written consent of K2.

Past performance is not an indicator or guarantee of future results.

Certain information contained in this document represents or is based upon forward-looking statements or information, including descriptions of anticipated market changes and expectations of future activity. K2 believes that such statements and information are based upon reasonable estimates and assumptions. However, forward-looking statements and information are inherently uncertain and actual events or results may differ from those projected. Therefore, too much reliance should not be placed on such forward-looking statements and information.

Professional care and diligence have been exercised in the collection of information in this document. However, data from third party sources may have been used in its preparation and Franklin Templeton/K2 has not independently verified, validated or audited such data.

Any research and analysis contained in this document has been procured by Franklin Templeton/K2 Investments for its own purposes and is provided to you only incidentally. Franklin Templeton/K2 shall not be liable to any user of this document or to any other person or entity for the inaccuracy of information or any errors or omissions in its contents, regardless of the cause of such inaccuracy, error or omission.

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of July 13, 2021, and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

The information in this document is provided by K2 Advisors. K2 Advisors is a wholly owned subsidiary of K2 Advisors Holdings, LLC, which is a majority-owned subsidiary of Franklin Templeton Institutional, LLC, which, in turn, is a wholly owned subsidiary of Franklin Resources, Inc. (NYSE: BEN). K2 operates as an investment group of Franklin Templeton Alternative Strategies, a division of Franklin Resources, Inc., a global investment management organization operating as Franklin Templeton.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Investments are not FDIC insured; may lose value; and are not bank guaranteed.