US Consumer Price Index (CPI) inflation jumped to a new high of 5.4% year-over-year (y/y) in June. This comes after a 5.0% rise in May and a 4.2% rise in April. Yet the US Federal Reserve (Fed), many investors and a number of economists still act unimpressed. They shrug and say, “it’s nothing, it will pass soon.” It’s beginning to remind me of the scene in Monty Python’s Holy Grail where the Black Knight, being hacked to pieces, insists “it is but a scratch, it’s just a flesh wound.” Those who claim inflation is no cause for concern are quick to point out the outliers: used car prices and gasoline prices were both up 45% y/y in June. They are outliers; but people do have to drive and new cars are hard to find these days, so these outliers hurt.

A quick look at Table 1 of the June US CPI release shows that significant y/y price increases were not limited to one or two items: transportation services were up 10%, car insurance 11%, apparel 5%, commodities other than food and energy close to 9%, and food away from home over 4%. Quite a few “flesh wounds.”1

I do not worry about 1970s-style runaway inflation. But investment strategy is mostly about understanding and assessing risk; and in a situation where markets and the Fed appear convinced that inflation will soon drop back under 2% by itself, with no need for policy action, the risks seem very much skewed to one side—namely that we might be underestimating inflation.

In assessing this risk, there are two factors worth considering, in my view.

The first is that after the high—and higher than expected—inflation readings of the last few months, high inflation will have a significant degree of inertia. White House officials have noted that excluding autos and pandemic-related services, June prices were up just 0.2% over the previous month, compared to the headline 0.9% month-over-month (m/m) jump. And 0.2% is the average m/m CPI increase during 2017–2019, the three years before the pandemic hit. But even if we assume overall inflation will drop to 0.2% already in July and stabilize at that rate, we will still have to wait until March 2022 for y/y inflation to drop consistently below 5%; at that stage inflation will have averaged 5% for a full 12 months (from April 2021–March 2022).

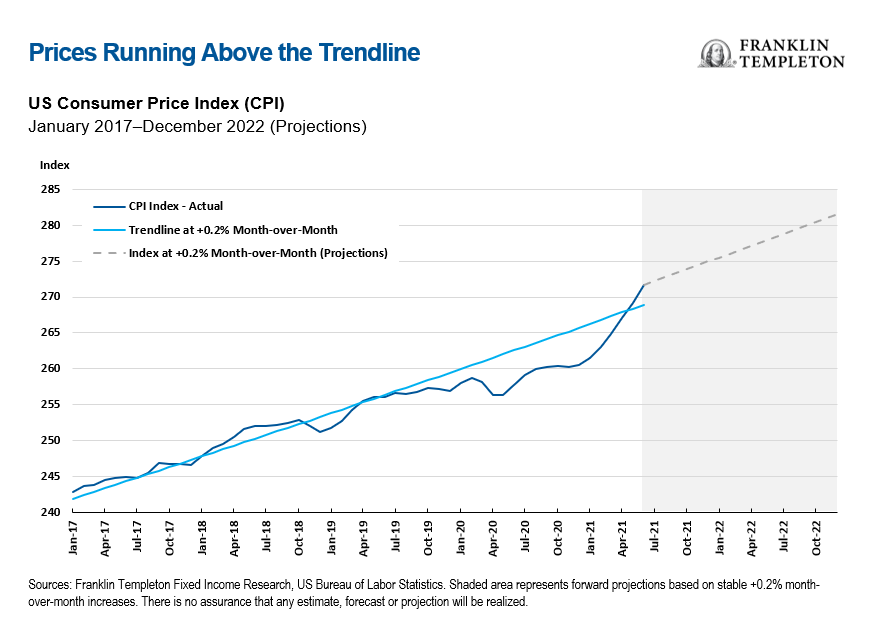

This, I repeat, assuming that inflation slows down immediately. Over the past four months, the average m/m increase has been 0.8%, pushing the CPI reading above the 0.2% trend line (beginning in January 2017 in the chart below). We have already more than fully made up for the price drops of last year’s lockdown. The longer the m/m rate runs above 0.2%, the longer annual inflation will remain elevated. And there are several factors that could contribute to monthly inflation readings above 0.2%: escalating housing costs, for example, are likely to feed into higher inflation contributions from owner equivalent rent.

Suppose as a worst-case scenario that inflation rises at 0.8% per month for another four months before reverting to 0.2%. Extremely unlikely, I know, but nobody expected it to average 0.8% over the past four months either. In that case inflation would fall just under 5% only in June next year; and before it does, it would run between 7.5% and 8.1% for five months, between October 2021 and February 2022.

The first thing to consider, therefore, is that the moderately high inflation we are experiencing now will likely persist for six to 12 months, and we might not have seen the worst; this could well have an impact on both inflation expectations and price-setting behavior.

Speaking of which, the second factor I want to highlight is the interesting dichotomy in inflation expectations. Those convinced that higher inflation will be short-lived are overwhelmingly in the ranks of central bankers and financial investors. By contrast, businesses and consumers are much more of the view that higher inflation will persist. A recent poll found that nine in 10 voters are worried about a rising cost of living. Corporate leaders have been warning that the disruptions and supply bottlenecks caused by the pandemic will take many more months to resolve.

I would love to think that financial investors are smarter and have a much keener insight into the future. But businesses and consumers who confront prices and price-setting decisions on a daily basis might deserve the benefit of the doubt on this one. Besides, they are the ones who will decide whether to pass on persistently higher input costs, and whether to bargain for higher wages after months of rising prices at the pump and in the shops—and in this tight labor market, workers do have bargaining power.

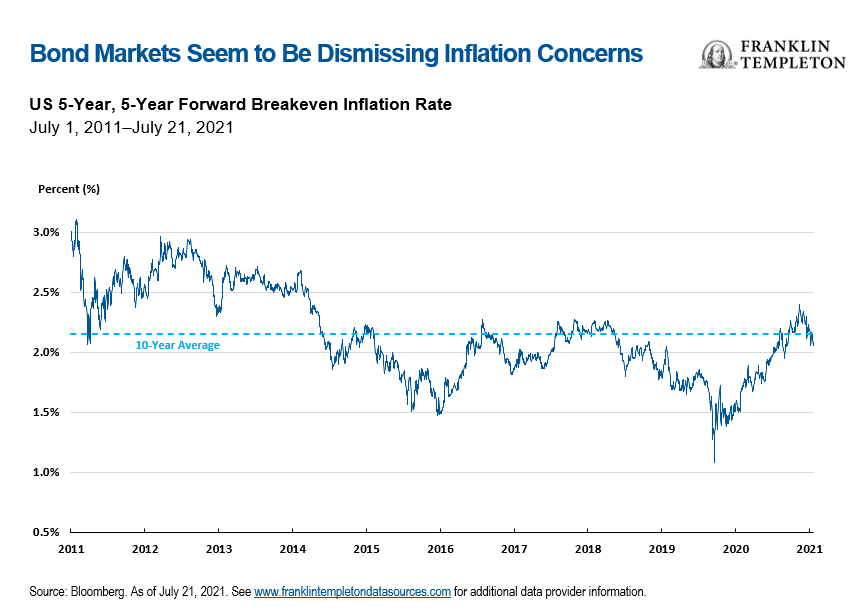

Moreover, the degree to which bond markets are dismissing inflation concerns is striking: five-year/five-year forward breakevens are below their 10-year average, and below where they were at the time of the eurozone debt crisis; ditto for the flatness of the yield curve. This to me suggests that the Fed’s heavy and reassuring presence in fixed income markets might be giving us a distorted view of what bond markets actually anticipate. Financial market measures of inflation expectations, in other words, might be a lot less informative than we think.

As I discussed in my previous On My Mind, there are three main possible macro scenarios ahead. Maybe the economy is about to tank; or maybe we are about to witness a productivity miracle. If not, all the signs suggest the bond market is underestimating the inflation risk.

Or maybe not. Maybe it’s just a flesh wound.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained herein has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Bond prices generally move in the opposite direction of interest rates. Investments in lower-rated bonds include higher risk of default and loss of principal. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Actively managed strategies could experience losses if the investment manager’s judgment about markets, interest rates or the attractiveness, relative values, liquidity or potential appreciation of particular investments made for a portfolio, proves to be incorrect. There can be no guarantee that an investment manager’s investment techniques or decisions will produce the desired results.

__________________________________

1. Source: Bureau of Labor Statistics. As of July 13, 2021.