Key takeaways:

- Macro uncertainties are currently elevated due to higher inflation, interest-rate increases, recession risks and the Russia-Ukraine war.

- Tightening financial conditions are putting pressure on property cap rates (one measure used to estimate and compare the rates of return for commercial or residential real estate properties). However, we believe sectors with strong fundamentals and properties with leases that are linked with inflation indexes, have a competitive edge in today’s environment.

- Secular and demographic-driven sectors look attractive to us because they tend to have stable cash flows, have less volatility and be more recession resistant.

- We also believe that environmental, social and governance (ESG) and social impact are a secular theme that will become an increasingly bigger investment mandate by institutional investors.

Macro uncertainties affecting real estate investing

The current macro environment is unique and complex with significant uncertainties. The COVID-19 pandemic disrupted daily life and normal market cycles. It also led to a synchronized global recovery, global inflation and central bank tightening. A synchronized global downturn seems likely as a result. It is possible that the United States and Europe will likely experience recessions later this year or early next year.

However, not everything is negative. Consumer spending, especially in Europe and the United States, has been holding up well. Strong household wealth, balance sheets and corporate earnings also appear encouraging. Leverage, especially in the banking system, is low compared to 2007 before the global financial crisis (GFC). For all these reasons, we believe a potential recession or downturn will not be as severe as the GFC. Consensus forecasts also show possible improvements in 2024.1

Inflation and rising interest rates

In our analysis, US inflation already peaked in June, and although it is currently a headwind for continental Europe, we believe eurozone inflation will likely peak soon. However, the pace of easing will depend on many factors and is hard to predict. Analyst predictions about the Russia-Ukraine war, which has impacted Europe much more than the rest of the world, range from Ukraine winning next spring to Russia launching a nuclear weapon. The global energy crisis has also hit Europe much harder than the United States and Asia, with natural gas mattering a lot more than crude oil. We believe this will be a big shock to the daily life and economy for Europe—even more so than in the 1970s. Global supply chain pressures seem to be moderating, but labor shortages will likely continue to have a negative impact, in our view.

Major central banks have been raising interest rates to curb demand and inflation, and we’ve seen rising bond yields. However, we believe that probably in the first half of 2023, there could be a pivot point where central banks may have to switch from quantitative tightening back to quantitative easing as signs of an economic slowdown or a recession become a reality. Meanwhile, we believe rising financing costs have resulted in market dislocation, which may present attractive acquisition opportunities in real estate over the next 12-18 months.

Effect of higher financing costs on real estate borrowing

The rise in interest rates has impacted real estate borrowing. For example, the Euro Interbank Offered Rate (Euribor) five-year interest rate swap has increased substantially in 2022.2 Higher financing costs have added upward pressure on cap rates and downward pressure on asset valuations.

In this environment, many investors prefer investing in assets that provide good current income and an inflation hedge. While inflation may not persist at the current 9%-10% range, it may stay around 3%-4% for a few years going forward. Therefore, inflation hedge is highly desirable.

Real estate offers opportunities for potential inflation hedging and diversification

With a volatile equity market and high inflation eroding the value of cash, many investors are searching for income with inflation-hedging characteristics. There is a lot of cash currently sitting on the sidelines; there is a record level of cash in the US money market in particular. In our opinion, the real estate asset class is an attractive option in today’s environment. For example, over the past 44 years, real estate total returns in the United States have consistently beat inflation.3

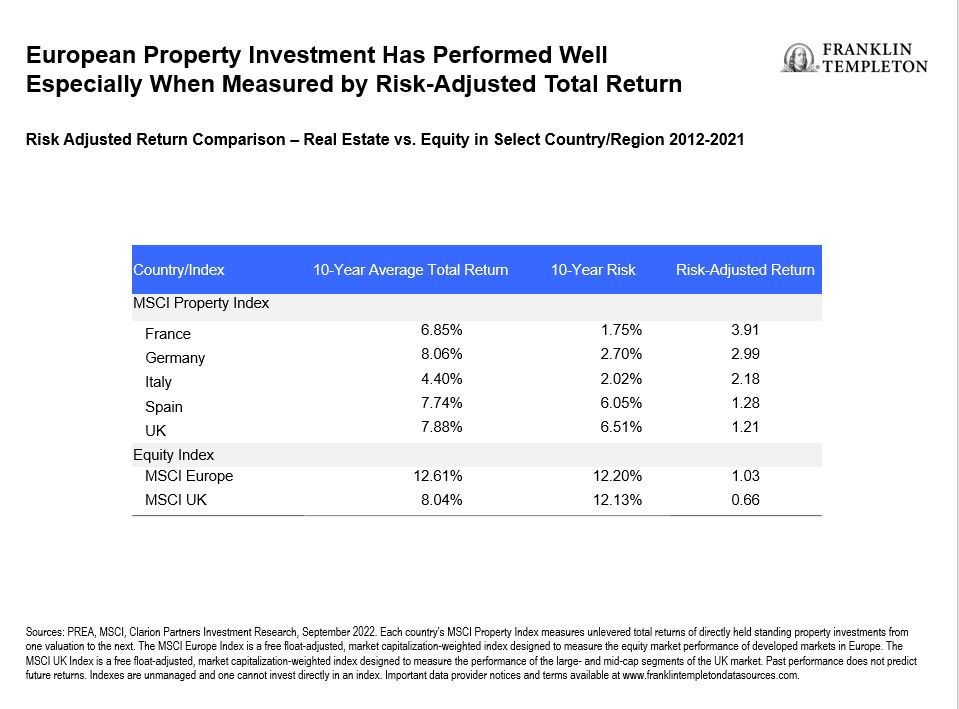

Commercial real estate in European countries has also generally provided better risk-adjusted returns than inflation over the past 10 years.4 So, European properties have provided good income as well as an inflation hedge.

There are typically two ways that real estate provides an inflation hedge. The first is when fundamentals are strong enough that landlords can raise rents, driving up property net operating income. One example of this includes the logistics sector, which has a low vacancy rate and high single-digit rental growth. Hotels are another example, benefiting from a wave of American tourists who are flocking to Europe to take advantage of the euro’s depreciation against the U.S. dollar.

The second way real estate can provide a hedge is through long-term leases linked to an inflation index, where landlords can pass on rising costs directly to their tenants. Examples include net leases (where a lessee pays a portion or all other property costs in addition to rent) as well as long-term leases in the health care, education and government sectors. Unlike in the United States, the majority of net leases in Europe have good lease terms linked with the country’s inflation index, making them an effective hedge in today’s market environment.

Additionally, real estate tends to be noncorrelated with stocks and bonds, and thus provides a potential diversification benefit.5

Secular sectors preferred in recessionary environments

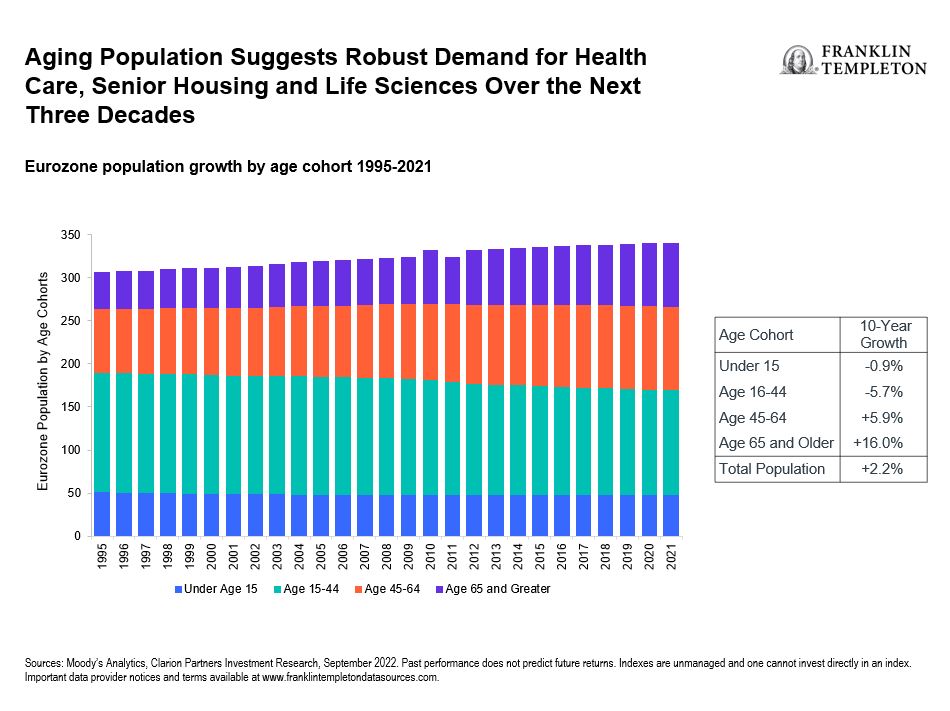

There are two types of real estate investment themes. The first is cyclical, where returns are tied to economic and job growth and boom-bust cycles. Real estate sectors that fall under this category include office, retail and traditional apartment housing. The second is secular, which tends to be related to demographics and disruptions. Secular investment themes have very little linkage to economic growth and can even be counter-cyclical. Additionally, these tend to be more recession resistant and experience lower volatility than cyclical investments. Aging populations worldwide represent an example of a demographic trend that benefits health care properties and senior housing.

ESG and e-commerce infrastructure also fall under the secular investment theme category. Social infrastructure, which includes health care, retirement/assisted living, affordable housing, social housing and student housing, ranks high among institutional investors.6

WHAT ARE THE RISKS?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stocks historically have outperformed other asset classes over the long term but tend to fluctuate more dramatically over the short term. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds adjust to a rise in interest rates, the share price may decline. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

The risks associated with a real estate strategy include, but are not limited to various risks inherent in the ownership of real estate property, such as fluctuations in lease occupancy rates and operating expenses, variations in rental schedules, which in turn may be adversely affected by general and local economic conditions, the supply and demand for real estate properties, zoning laws, rent control laws, real property taxes, the availability and costs of financing, environmental laws, and uninsured losses (generally from catastrophic events such as earthquakes, floods and wars).

Investments in alternative investment strategies are complex and speculative investments, entail significant risk and should not be considered a complete investment program. Depending on the product invested in, an investment in alternative investments may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment.

Franklin Templeton and our Specialist Investment Managers have certain environmental, sustainability and governance (ESG) goals or capabilities; however, not all strategies are managed to “ESG” oriented objectives.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

__________

1. Source: Bloomberg as of September 21, 2022. There is no assurance that any estimate, forecast or projection will be realized.

2. Sources: Bloomberg, Clarion Partners Investment Research, September 2022.

3. Sources: NCREIF, Bureau of Labor Statistics, Bloomberg, Clarion Partners Investment Research, as of Q2 2022. Past performance is not an indicator or a guarantee of future results.

4. Sources: PREA, MSCI, Clarion Partners Investment Research, September 2022.

5. Diversification does not guarantee profit or protect against the risk of loss.

6. Sources: PwC/ULI Emerging Trends in Real Estate Europe 2022, Clarion Partners Investment Research, September 2022.