Originally published in Stephen Dover’s LinkedIn Newsletter Global Market Perspectives. Follow Stephen Dover on LinkedIn where he posts his thoughts and comments as well as his Global Market Perspectives newsletter.

In shipping, the “final mile” refers to the end delivery point. In climbing, it refers to the most arduous ascent to the peak. No matter the context, the final mile is the culmination of a worthy endeavor.

In the context of fighting inflation, the “final mile” represents the successful and sustainable achievement of a central bank’s inflation target. For the Federal Reserve (Fed), which began tightening monetary policy in 2022 when core personal consumption expenditures index inflation peaked at 5.8%, the final mile represents the challenge of bringing it down from its current rate of 3.7% to its 2% target.

As worthy as the objective is, the final mile can come at significant cost. At altitude, oxygen is depleted and muscles ache. In transportation, goods must be offloaded from larger to smaller trucks at considerable cost.

Is the same true for monetary policy? Is the final mile the costliest part of restoring price stability?

According to Fed Chairman Jerome Powell, the answer is most likely “yes.” If that is true, are markets prepared for the hardship? Based on current pricing in stocks, bonds and currencies, the answer is “probably not.”

How the Fed sees the final mile

Perhaps the biggest surprise in macroeconomics this year has been the resilience of the US economy and its labor market following aggressive Fed tightening since early 2022. Despite dire warnings from most economists, supported by classic “leading indicators” of recession—such as an inverted yield curve—the US economy has motored ahead. If anything, over the past two years growth has exceeded its trend. Job gains have exceeded the growth of the labor force,1 resulting in five-decade low unemployment rates.

Falling inflation across all measures (core, headline, consumer prices and wages) has accompanied strong growth and a tight labor market. So why must the final mile—the achievement of the Fed’s 2% inflation target—be painful?

That is an important question. The Fed’s consistent message over the past year has been that a fall in inflation to its target will require a period of below-trend growth. Put differently, the Fed believes that for inflation to sustainably complete its desired decline, some slack must emerge across the economy, and particularly in the labor market.

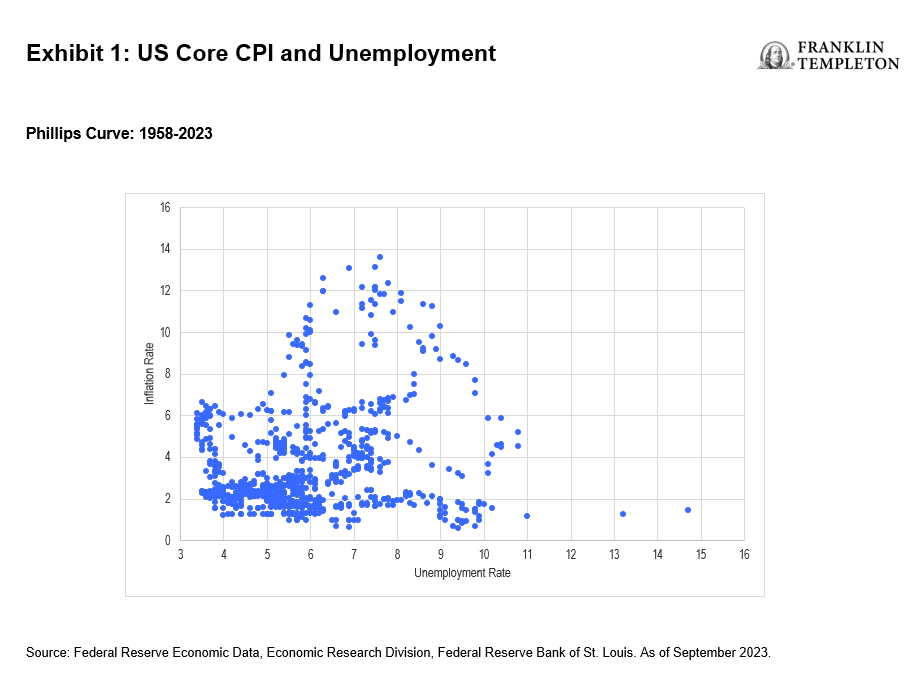

That notion hinges on an apparent empirical regularity first published in 1958 by the New Zealand economist William Phillips. The eponymous “Phillips Curve” purports to show a trade-off between inflation and the rate of unemployment. Specifically, inflation is high and rising when unemployment is very low, and inflation typically declines when unemployment is elevated.

The Fed’s Phillips fascination

Powell has clearly stated that some slack in the economy will probably be needed to achieve lasting low inflation. In his recent remarks before the Economic Club of New York, Chairman Powell noted:

“…the record suggests that a sustainable return to our 2 percent inflation goal is likely to require a period of below-trend growth and some further softening in labor market conditions.”2

There are, however, at least two odd aspects to that statement. First, as indicated in Exhibit 1 below, no statistically meaningful relationship exists between US inflation and the unemployment rate over the past 65 years. That is true even when adjusting for lags between unemployment and inflation, or when using the gap between realized unemployment and its estimated equilibrium rate.

Second, as noted above, Powell’s statement seemingly dismisses the fact that US measures of core and headline inflation, as well as wage inflation, have all declined sharply over the past 12 months without a period of significant below-trend growth, much less a significant increase in unemployment.

So why is the Fed insistent that sustainably achieving its 2% inflation target will require below-trend growth and rising unemployment?

Several factors likely enter the Fed’s thinking.

- First, there is a widespread perception, to some extent backed up by recent data, that declines in inflation will slow or even stall before the 2% target is reached. One such area of concern today is stubborn core services inflation, excluding rents.

- Second, while wage inflation has slowed, its current pace of 4.4% (average hourly earnings) or 4.3% (Employment Cost Index basis) is considered above what is consistent with 2% core price inflation. For instance, if trend productivity growth averages 1% per annum (a reasonable estimate), then wage (and benefit) inflation would have to fall by a further percentage point for price stability to ensue.

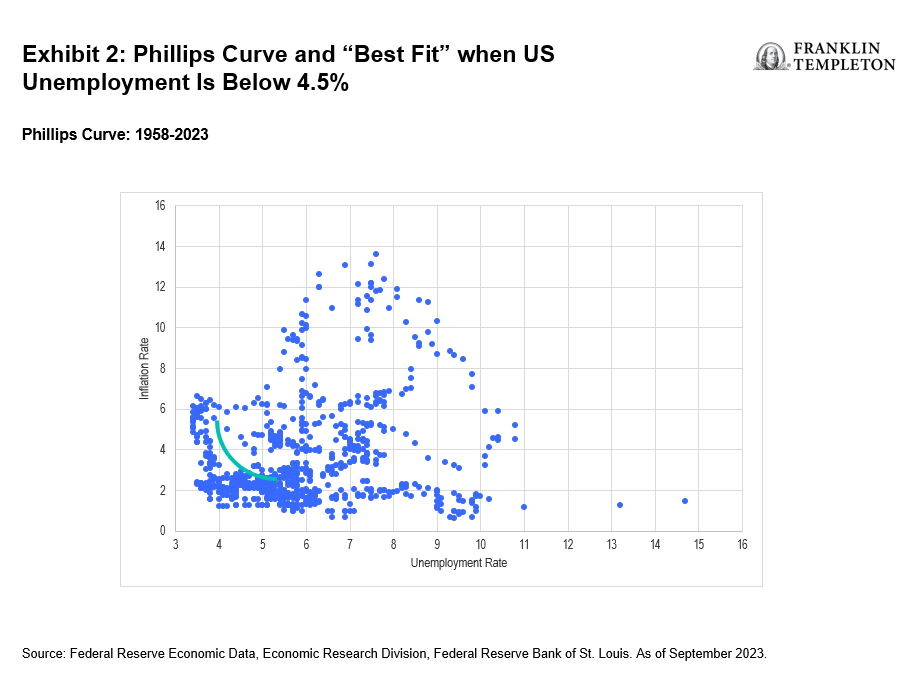

- Third, as shown in Exhibit 2, below, there may be a Phillips Curve trade-off when the unemployment rate falls below 4.5%. That is shown in the diagram by the curved line of best fit. If so, then getting inflation down the final mile may require some rise in the unemployment rate from its current level (3.7%). Indeed, using regression techniques to measure the trade-off between unemployment and inflation when the unemployment rate is below 4.5% indicates that for every 0.1% increase in the unemployment rate, the year-over-year Consumer Price Index (CPI) core inflation rate falls by 0.3%.

- Finally, the Fed appears to have greater loss aversion to above-target inflation than to too much unemployment. Partly, that stems from long-term credibility concerns. Persistent inflation overshooting could lead to a rise in long-term inflation expectations, which might be costly to undo. And the Fed’s asymmetric loss aversion may also reflect the harsh criticism it endured when it suggested in 2021 that inflation would be ”transitory.” It doesn’t want to repeat that communications gaffe.

Implications for markets

In sum, the Fed appears determined to maintain sufficiently restrictive monetary and financial conditions until economic growth slows below its trend rate and unemployment rises. Moreover, if those outcomes do not emerge soon, the Fed appears prepared to hike rates even further.

Are these outcomes consistent with current market expectations?

With respect to US and global equities, the Fed’s baseline scenario presents a challenge to prevailing earnings expectations. The consensus of company analysts has boosted its S&P 500 profits forecast for 2024 to 11.9% growth.3 Should a growth slump below trend happen next year, earnings will likely turn out to be closer to flat, at best. If the economy dips into recession, earnings could fall outright.

Recently, US bond yields have tumbled. But they remain a full percentage point above their levels from earlier this year, boosted by growth surprises and heavy Treasury issuance. If US economic growth stumbles in the coming quarters, bond yields are likely to fall even further.

Finally, in 2023 the US dollar has appreciated strongly, supported by higher US bond yields and wider interest differentials relative to other countries. Those twin sources of support will recede if the Fed gets its way, likely leading to a weaker dollar in 2024.

In sum, investors risk underestimating the resolve of the Fed to engineer below-trend economic growth and rising unemployment to achieve its inflation target. A harsher-than-expected recession is likely. As a result, US equity markets and the dollar appear vulnerable. The first five years of the US Treasury curve remain too optimistic about Fed easing; in our view, rate cuts will probably occur later and more gradually than is currently priced into the market. We believe the longer end of the yield curve (10 years and beyond) which is more sensitive to the long-term growth, inflation and financial implications of extended Fed tightening, offers better value, given the likely downward pressure on medium-term growth and inflation expectations that the Fed’s resolve implies.

The final mile is often the most difficult. While we hope that adage does not result in significant economic hardship in regard to the US monetary policy, we also recognize that hope is not a strategy. Investors may need to prepare for a difficult final ascent.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

__________

1. Source: “Labor force and macroeconomic projections overview and highlights, 2022–32.” US Bureau of Labor Statistics. September 2023.

2. Source: Board of Governors of the Federal Reserve System. October 19, 2023.

3. Source: FactSet, as of November 10, 2023. There is no assurance that any estimate, forecast or projection will be realized.