Key takeaways:

- This year’s pronounced divergence in market performance presents an opportune time for investors to consider tax-loss harvesting strategies with single-country exchange-traded fund (ETF) allocations.

- A key consideration in tax-loss decision-making is whether a comparable or highly correlated ETF exists at a lower cost for those seeking to maintain desired exposures to chosen markets with attractive long-term prospects.

- For many investors, international markets are still underrepresented in their portfolio allocations. Global stocks, however, offer potential diversification benefits and many have favorable characteristics that offer differentiated long-term opportunities. Japan, for example, has seen improving governance boost company profits and attract foreign investors with increased buybacks and dividends.

With U.S. technology mega cap’s dominant role in the S&P 500 Index’s rally this year and the anti-climactic reopening of China from its zero-COVID policy, many investors have shied away from increasing their global equity exposure. As of the end of September, global equity funds saw net outflows of $10.65 billion.1

However, in our opinion, certain markets benefit from positive macro and geopolitical catalysts, combined with longer-term trends that favor equities abroad, and some of 2023’s underperforming holdings may be prime candidates for tax-loss harvesting.

A silver lining to down markets

To begin with some clarity on tax-loss harvesting, investors should be aware that it is applicable to a variety of investments, including individual equity securities, mutual funds and ETFs. Investors can shed underperforming investments for losses in taxable accounts and incur lower net capital gains—a key consideration for those seeking to maintain desired exposures, including allocations to global markets with attractive long-term prospects. To that end, it’s worth looking into comparable or highly correlated investments available at a lower cost. Keep in mind, however, the Internal Revenue Service’s wash-sale rule prevents a loss being taken on the sale of any security swapped for a substantially identical one within the same 30-day period.

To increase portfolio diversification, one viable approach includes shedding underperforming individual holdings in favor of single-country ETFs. Index-based ETFs are generally low-cost, tax-efficient vehicles that investors buy and sell on a secondary market. Investor redemptions from ETFs generally do not create taxable events for remaining shareholders, which can make a difference in returns over the long term. While ETFs are not entirely without tax drag (the reduction of potential income due to taxes), index ETF managers proactively look for opportunities to minimize capital gains.

Eye on China

If an investor’s portfolio took a hit when China’s property sector was reeling, consider that recent data from the country’s National Bureau of Statistics (NBS) showed two consecutive months of profit gains for Chinese industrial firms, signaling that supportive government measures may be working to stabilize the economy. China’s economy saw a 11.9% year-on-year rise followed an unexpected 17.2% gain in August, alongside September’s stronger-than-expected industrial and consumption activity.2

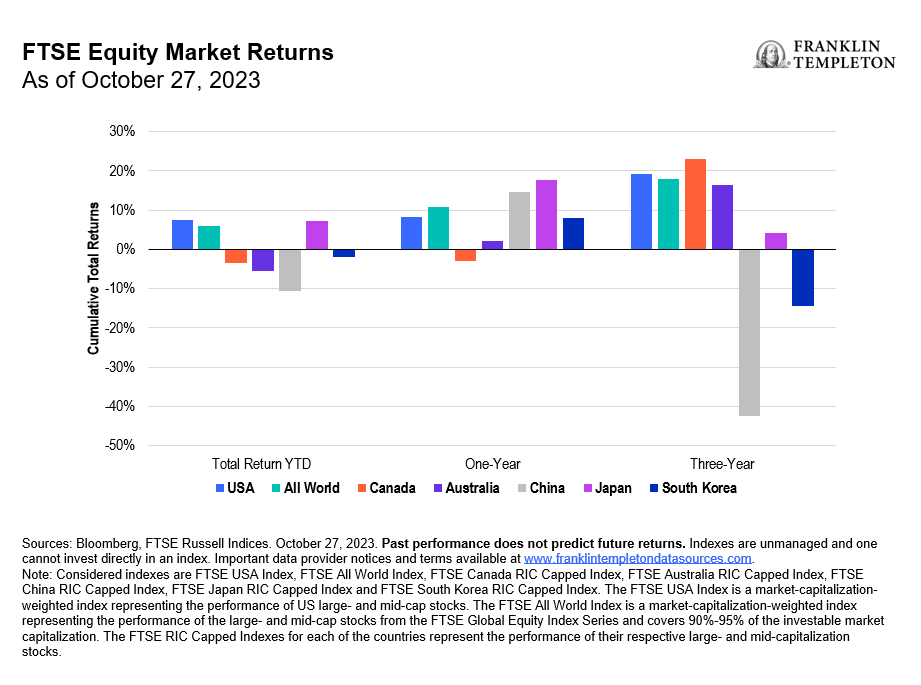

With the MSCI China Index down about -11% as of the end of October, China’s market seems a prime target for tax-loss selling. However, rather than channeling investment out of emerging markets like China entirely, we believe investors should temper excessive pessimism to such deeply discounted markets. In China’s case, its decades-long story of unprecedented economic success has stemmed largely from its adoption of a market-driven economy, which remains intact as a source of dynamism and opportunity. More direct flights between the United States and China have resumed. And there are encouraging signals of improved goodwill and cooperation as President Joe Biden and President Xi Jinping conclude their Bay Area meeting. We believe this makes for a compelling case for capital redeployment in the tax-loss harvesting process and the compounded cost savings over time when investors switch into a comparable lower-fee product.

China still has vast and still-untapped human capital, capable of producing a highly trained and motivated workforce. It also offers an enormous domestic market that creates strong incentives for investment and innovation with the ability to significantly boost new industries rapidly. We are seeing this with the country’s constructive Generative AI policies—just like the quick rollout of policy frameworks that accelerated its electric vehicle and solar markets.

Maintaining global equity exposure

While the emerging market asset class has lagged developed markets this year, investors should keep in mind that dispersion in the returns of single-country indexes have historically been as wide as 50%, highlighting the potential benefits of a diversified portfolio.

High-growth emerging markets with burgeoning middle-class consumers also have the potential to grow more rapidly than advanced economies. The International Monetary Fund (IMF) forecasts 2023 real gross domestic product (GDP) growth of about 4% for emerging and developing countries, helped by economies such as India, which is expected to grow at a rate of 6.3%.3

And, in our analysis, emerging market equities offer good value—as they are priced at a discount to developed markets. Brazil’s attractive stock valuations are expected to continue luring in foreign capital, while expanding exports may continue to favor its currency. As we recently wrote, we view Brazilian equities as substantially undervalued, with price-to-earnings (P/E) ratios for the last 12 months (LTM P/Es) in the mid- to high-single digits, constituting a material discount to both emerging and developing markets. Tax-loss harvesters should also look broadly at the region and consider how well Latin America has weathered recent global shocks.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. The government’s participation in the economy is still high and, therefore, investments in China will be subject to larger regulatory risk levels compared to many other countries.

ETFs trade like stocks, fluctuate in market value and may trade above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns. ETF shares may be bought or sold throughout the day at their market price on the exchange on which they are listed. However, there can be no guarantee that an active trading market for ETF shares will be developed or maintained or that their listing will continue or remain unchanged. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

For more information on any of our funds, contact your financial advisor or download a free prospectus. Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. The prospectus contains this and other information. Please read the prospectus carefully before investing or sending money.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon, by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute

__________

1. Source: Morningstar. As of September 30, 2023.

2. Source: China NBS.

3. IMF forecasts as of October 2023. There is no assurance that any estimate, forecast or projection will be realized.