Value stocks are magnificently ordinary. Not only are they in less flashy sectors like consumer staples, industrials and health care, but they also are trading at historically reasonable valuations. That might be advantageous to investors in what could be an uncertain 2024 when investors could face higher volatility among expensive growth stocks, normalizing interest rates and the further unwinding of pandemic-era stimulus. Such an environment may make these ordinary value companies look extraordinary.

Value’s valuations matter

Although value stocks have lagged their growth counterparts over much of 2023, we believe the set up for 2024 and beyond looks promising. Historically, starting valuations have been a strong indicator of long-term future returns.

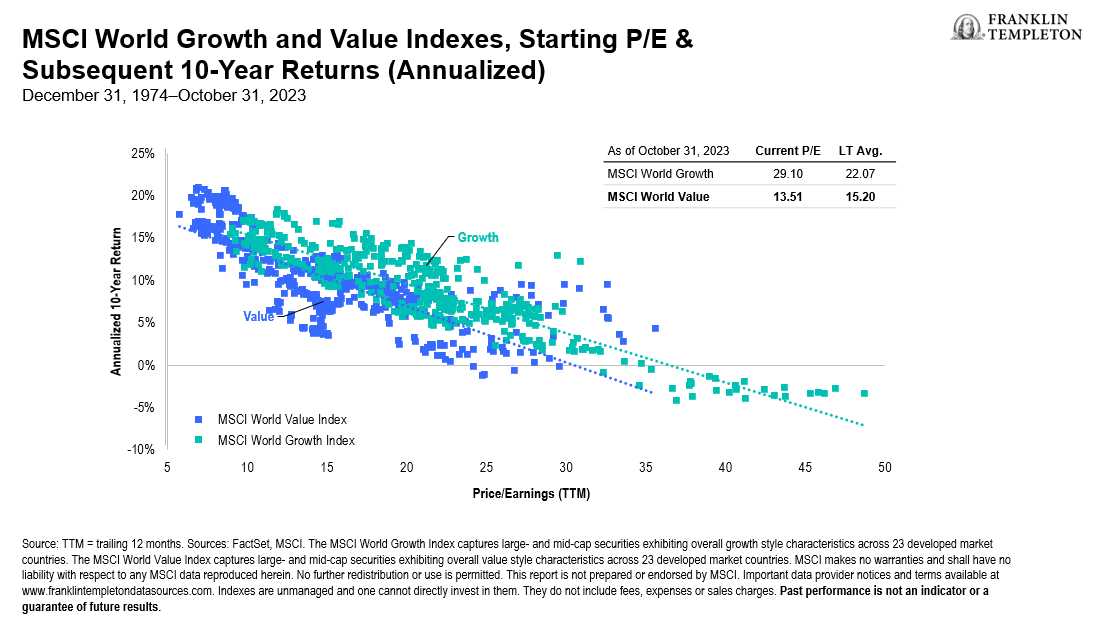

Currently, the MSCI World Value Index’s price-earnings (P/E) multiple is trading at a discount to its historical average, whereas the P/E multiple for the MSCI World Growth Index is at premium. As seen in Exhibit 1, comparing the trailing P/E multiples for global growth and value stocks with their return over the next 10 years shows that lower P/E stocks achieved higher future returns over the next decade, based on data from FactSet and MSCI. As such, with growth stocks’ stretched valuations, we see many opportunities to find compelling value opportunities with significant future return potential.

Exhibit 1: Valuations Matter for Long-Term Returns

Furthermore, we believe that finding companies with compelling catalysts that can unlock value and generate solid long-term returns will remain crucial for separating appealing value stocks from potential value traps, particularly in an environment of increasing uncertainty. We also think the market should reward stable cash flow generation and financial returns. We believe it’s important to focus on cash flows and financial returns to understand how a company is run and whether it can produce strong share price appreciation for investors over time.

Diversification over concentration

With 2023 global market returns concentrated in a handful of US stocks, seeking out value stocks can give investors more diversified global exposure and potentially more consistent returns over time, in our view.

We tend to think the world outside the United States has more opportunities. While we do see some US prospects, when we look at Europe, for example, we can find big globally competitive companies that are trading at compelling valuations and provide the potential opportunity for attractive future returns.

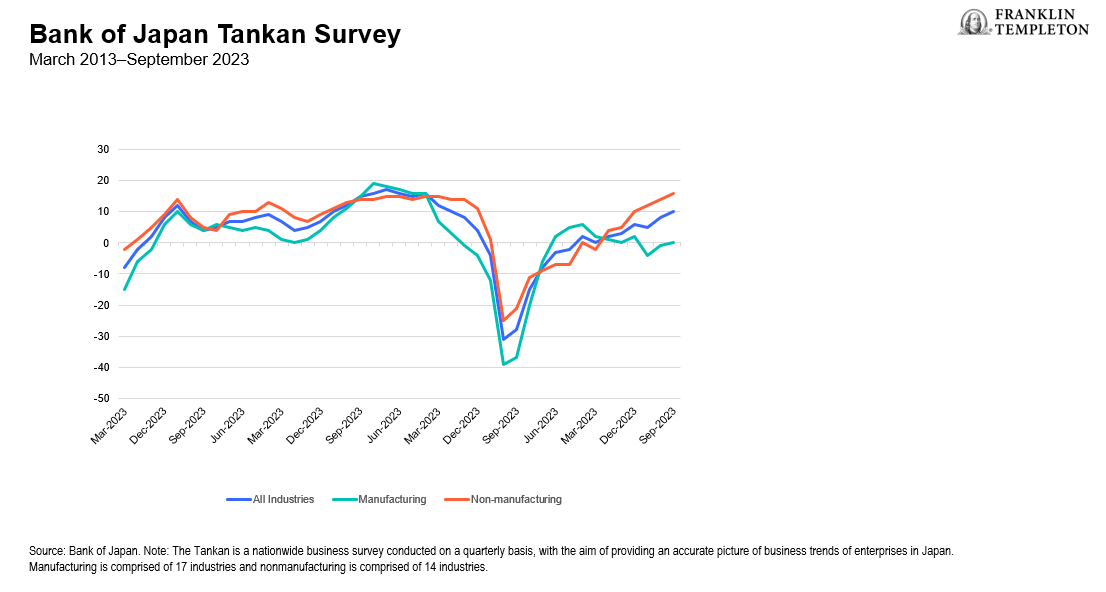

Japan is also an increasingly dynamic market worth investors’ attention, in our view. More and more Japanese companies are focused on improving returns on capital, raising prices amid higher inflation and are willing to take more risks to pursue faster growth—a marked change from the past few decades. The Tokyo Stock Exchange is also pushing reforms to get companies to raise their book values.

Despite a strong performance this year, Japanese stock valuations (based on FactSet data) remain attractive to us, as the country exits a long period of negative interest rates and overall business sentiment continues to improve (Exhibit 2).

Exhibit 2: Bank of Japan Tankan Judgment Survey Shows Growing Corporate Optimism

Monetary policy normalization in many countries should further positively impact certain value-oriented sectors. Higher interest rates have lured capital away from dividend-paying industries toward fixed income over the past year. For value investors, the drop in valuations in the consumer staples, utilities and real estate sectors, for instance, can create greater prospects of finding stocks unfairly trading below their fundamental value.

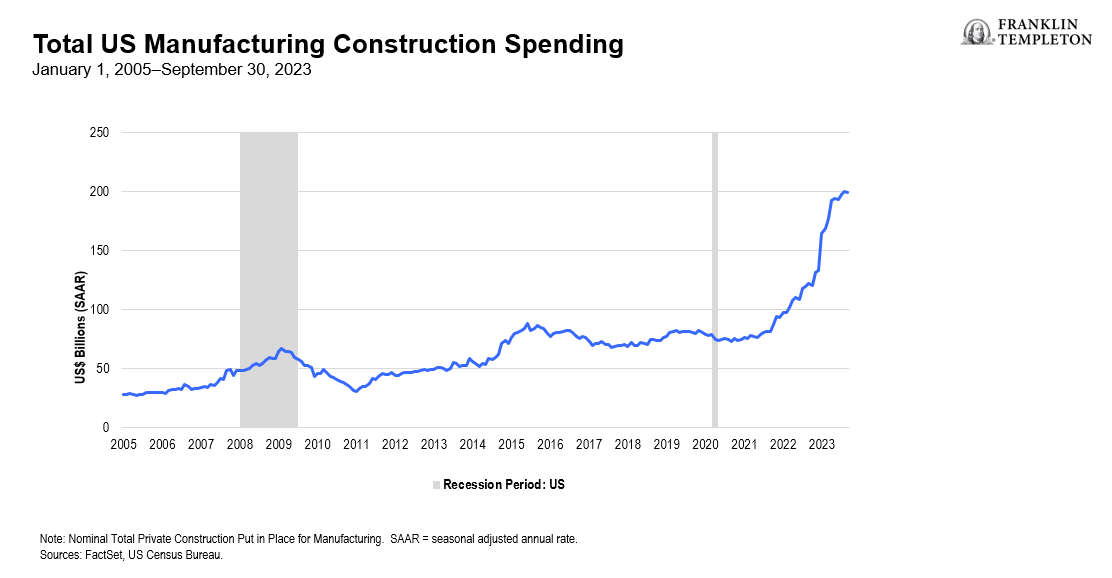

Government infrastructure spending and the long-term energy transition is also geared toward sectors that trade at “value” multiples, such as companies in the energy, industrials and materials sectors. US government spending on building new semiconductor and electric vehicle battery plants, for one, should lead to greater spending on the metals, cement and industrial equipment used to build them. US spending on manufacturing facilities has risen sharply since recent legislation was passed in Congress. (See Exhibit 3.)

Exhibit 3: US Stimulus Infrastructure Spending Booms

Momentum behind the energy transition also continues to push energy companies and utilities toward embracing cleaner energy. While we do not think oil is going away, global utilities are closing coal plants and rolling out renewable projects, incentivized by a slew of recent legislation in the United States and in Europe.

Pandemic’s end

Consumer spending is an area of concern. While growth has slowed as Americans spend the last of their pandemic-era savings, student loan repayments are restarting and low-end consumers are dealing with higher energy costs. We believe what is happening is only a spending slowdown, not a shutdown.

The labor market has so far remained resilient with increased participation, rising wages and persistently low unemployment supported by continued business and government infrastructure spending. However, should wages, employment or the promised infrastructure spending falter, we would not be surprised to see an economic slowdown.

Regardless, after a year when value underperformed growth stocks globally, we anticipate a brighter year ahead as global stock valuations suggest to us positive long-term return potential. More money should also flow to value-oriented parts of the market and economy through ongoing consumer spending and recent government programs, while normalized monetary policy can make interest rate sensitive and dividend-paying groups more appealing. Extraordinary value. Extraordinary potential.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

To the extent a strategy invests in companies in a specific country or region, it may experience greater volatility than a strategy that is more broadly diversified geographically.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Value securities may not increase in price as anticipated or may decline further in value. The investment style may become out of favor, which may have a negative impact on performance.

Active management does not ensure gains or protect against market declines.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.