Many of the same factors that impact traditional investments also impact alternative investments. Some provide headwinds while others provide tailwinds. For example, higher interest rates can favor private credit because of the floating-rate nature of most of the debt. On the other hand, they may hurt commercial real estate as credit conditions tighten, and they can negatively impact private equity due to the rising cost of capital to finance transactions.

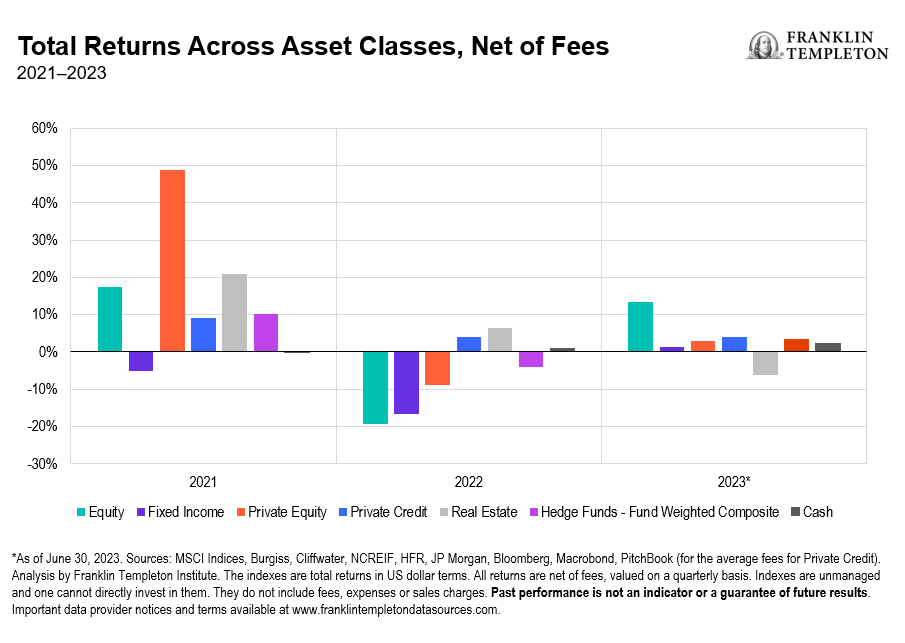

As we examine the performance of traditional and alternative investments over the last three years (Exhibit 1), we can see strong results in 2021 as the market peaked, then a sharp reversal in 2022, and a rebound in 2023. This short window illustrates the differences across asset classes, with public equity losing more in 2022 but recovering more rapidly than private equity in 2023. After a strong 2021, real estate delivered positive results in 2022, but lagged in 2023 due to rising interest rates and falling occupancy in the office space sector.

Exhibit 1: Total Returns Across Asset Classes (right click on chart to enlarge)

We summarize the challenges and opportunities below. As capital is allocated in 2024, note the distinction between putting capital to work today versus that which was committed prior to 2021, peak valuations for private markets.

Private commercial real estate

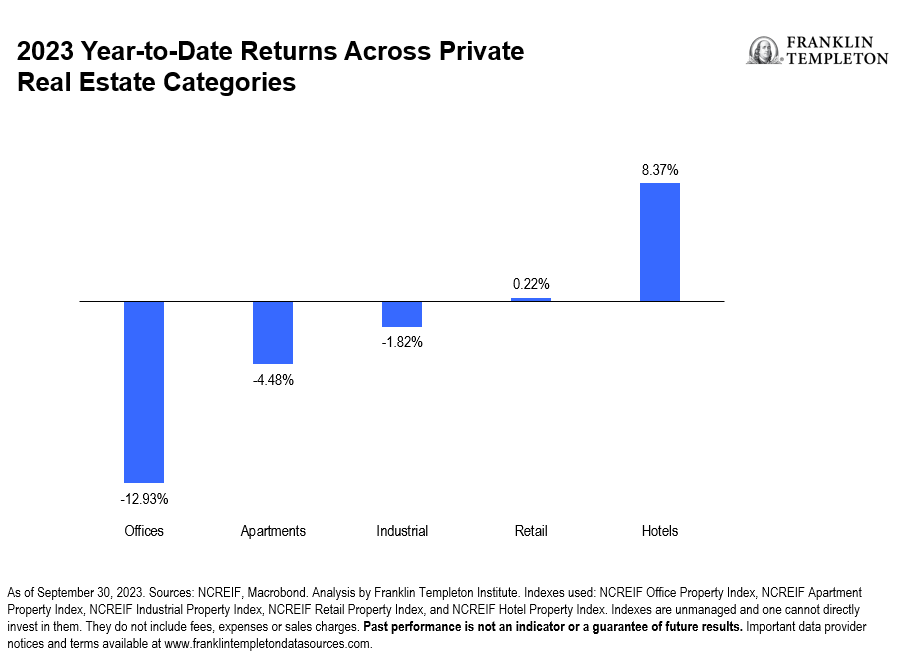

Commercial real estate had a challenging 2023 (Exhibit 2), with the office sector down nearly 13% through September, and apartments down nearly 4.5%. Even the industrial sector, which has performed well over the last several years, was down nearly 2%. Hotels have been the best-performing sector, up over 8% through September. Rising interest rates, and concerns regarding financial contagion post-Silicon Valley Bank (SVB), have created a challenging environment for many real estate sectors.

Exhibit 2: A Challenging Year for Commercial Real Estate (right click on chart to enlarge)

Headlines have focused on challenges to the office sector, as it faces headwinds for the foreseeable future. We believe there may be opportunities for lenders who can renegotiate terms. In addition, we see attractive opportunities in industrials, multifamily and life sciences.

While the office sector has lagged, the industrial sector has delivered strong results, buoyed by a growth of warehouses and fulfillment centers.

Private credit

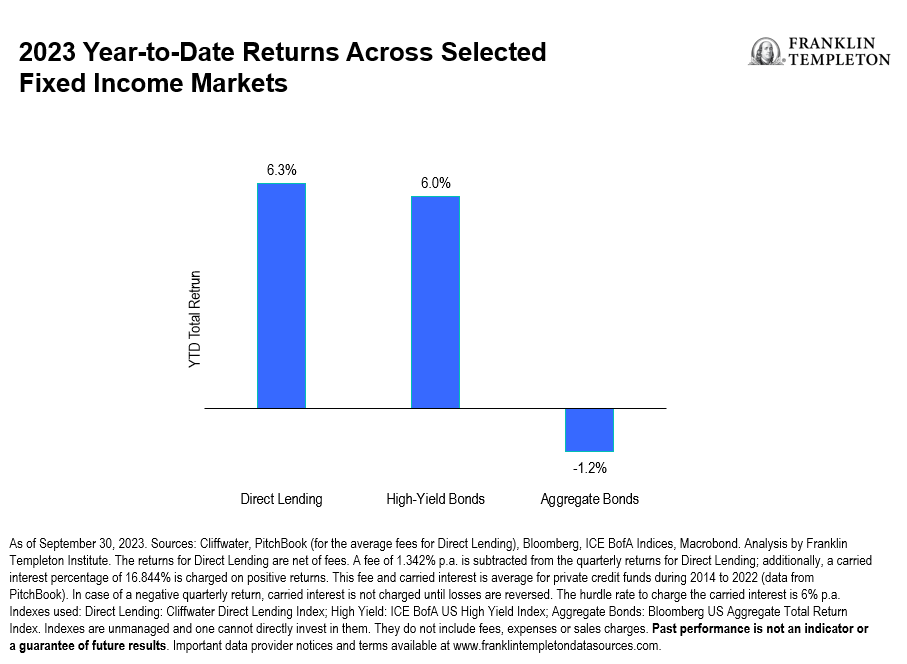

Broadly private credit had a good year in 2023, mitigating the rise in interest rates with mostly floating-rate debt. In fact, most risk assets, including direct lending and high yield, provided attractive returns (Exhibit 3). Given strong economic growth defaults were limited, but that could change in the coming year.

Exhibit 3: A Good Year for Private Credit (right click on chart to enlarge)

Looking at 2024, the potential for a slowing global economy could affect the outlook for existing private credit investments and lead to more defaults. For new investors, 2024 could present new opportunities. For example, the SVB collapse created a significant opportunity as banks retrenched from lending to small and middle market companies.

As the pendulum has shifted towards nonbank lenders, seasoned private credit managers may be able to lend capital at favorable rates and terms. As banks are less willing to lend, companies will need to refinance, giving private equity investors the opportunity to negotiate good returns and covenants.

Private equity

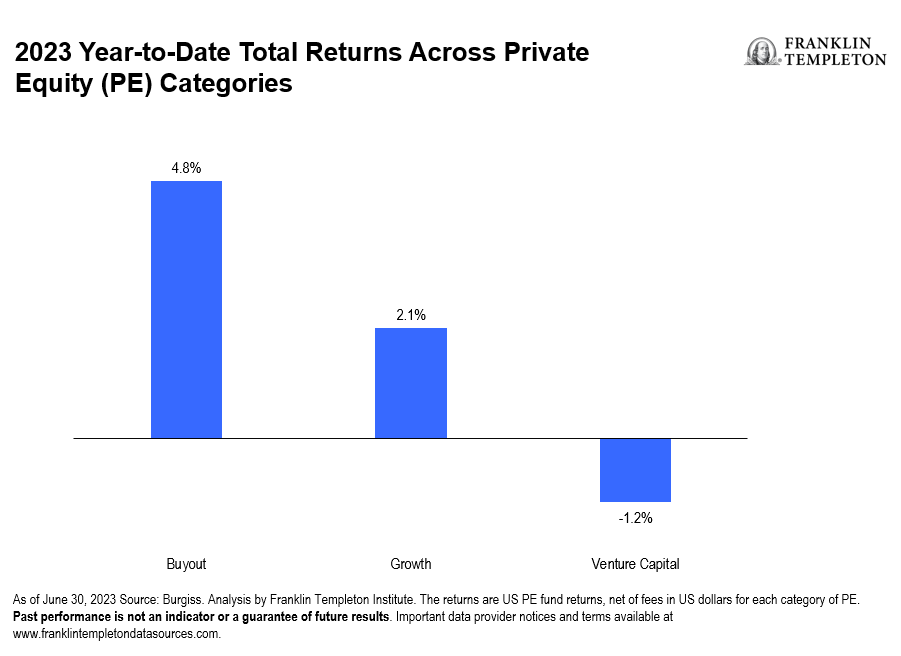

Private equity experienced mixed results in 2023, with buyouts and growth equity delivering positive results, and venture delivering negative returns through June (Exhibit 4). Performance hasn’t been the issue for private equity; it has been the lack of activity, and the overallocation by many institutions.

Exhibit 4: Mixed Results for Private Equity in 2023 (right click on chart to enlarge)

Coming out of a challenging 2022, many institutions found themselves overallocated and overcommitted to private equity. This has been referred to as the “denominator effect,” as institutions found themselves overallocated to alternatives due to the decline in value of their public market positions relative to private markets. The overallocation was exacerbated by the dramatic slowdown of exits, and existing commitments to private equity.

This presented an unprecedented opportunity to secondaries managers who were able to provide liquidity to institutions. Managers were able to select prized assets at favorable valuations, and then assemble portfolios diversified by industry, geography, and vintage. By diversifying their vintage years, they were able to shorten the J-curve, and potentially distribute capital to investors sooner. We believe this trend will continue.

Summary

In the coming year, we see both challenges and opportunities for allocating capital to alternative investments. To learn more, please register for our upcoming Alternative Investment Outlook podcast and visit our website for additional materials (alternativesbyft.com).

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Investments in many alternative investment strategies are complex and speculative, entail significant risk and should not be considered a complete investment program. Depending on the product invested in, an investment in alternative strategies may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. An investment strategy focused primarily on privately held companies presents certain challenges and involves incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity. Diversification does not guarantee a profit or protect against a loss.

Risks of investing in real estate investments include but are not limited to fluctuations in lease occupancy rates and operating expenses, variations in rental schedules, which in turn may be adversely affected by local, state, national or international economic conditions. Such conditions may be impacted by the supply and demand for real estate properties, zoning laws, rent control laws, real property taxes, the availability and costs of financing, and environmental laws. Furthermore, investments in real estate are also impacted by market disruptions caused by regional concerns, political upheaval, sovereign debt crises, and uninsured losses (generally from catastrophic events such as earthquakes, floods and wars). Investments in real estate related securities, such as asset-backed or mortgage-backed securities are subject to prepayment and extension risks.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

An investment in private securities (such as private equity or private credit) or vehicles which invest in them, should be viewed as illiquid and may require a long-term commitment with no certainty of return. The value of and return on such investments will vary due to, among other things, changes in market rates of interest, general economic conditions, economic conditions in particular industries, the condition of financial markets and the financial condition of the issuers of the investments. There also can be no assurance that companies will list their securities on a securities exchange, as such, the lack of an established, liquid secondary market for some investments may have an adverse effect on the market value of those investments and on an investor’s ability to dispose of them at a favorable time or price. Past performance does not guarantee future results.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Copyright © 2024 Franklin Templeton. All rights reserved.