Demographics as a driver of economic growth

Conventional wisdom points to young demographics being a driver of economic growth. The thesis is that young populations indicate a growing labor force, suggesting productivity gains long into the future. The reality is more complicated.

Many observers say China’s shrinking population is an indicator of the country’s economic slowdown. However, populations that are educated can fight the negative impact of aging via retraining and adapting the workforce to new technologies. In China, every two workers who retire will have had around six years of formal schooling. They are being replaced by 1.6 young people with around 14 years1 of formal schooling. The country is upskilling its labor force by default.

Having a lot of young people is clearly good, but they need to be healthy enough to work and able to learn the skills that are in demand in the labor market. We don’t need millions of Ph.D.s—but rather, a relatively well-educated pool of young people, because they are more easily employable. Given the trend toward automation and artificial intelligence (AI), the growth of the “knowledge” economy drives demand for skilled workers. A young, well-educated labor force tends to attract investment in high margin, productive areas, providing the positive driver for economic growth.

Pensions and healthcare

A wave of liabilities is growing around the world, driven by aging populations that imply significantly higher healthcare and pension costs. It is not about the number of young people; we think it is policy direction that matters. Governments that implement policies to encourage savings for pensions and invest in healthcare provision are less likely to be challenged.

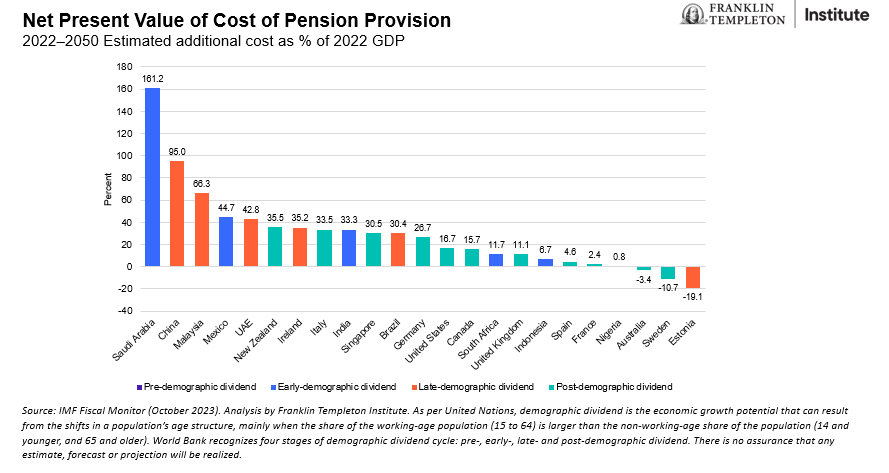

Exhibit 1 illustrates the incremental cost of pension provision up to 2050, expressed as a percentage of 2022 gross domestic product (GDP). The colors denote each country’s position away from that optimum point of “demographic dividend.”2

Exhibit 1: The Economic and Fiscal impact of Aging Populations

“Early demographic dividend” countries also risk significant growth in liabilities in the next generation. For example, Saudi Arabia has a relatively young population and needs to finance the equivalent of over 160% of 2022 GDP to pay for pensions provision by 2050. China, a giant economy with a shrinking population and a liability of 95% of 2022 GDP, is another example. The impact of policymaking is very clear in the few countries we highlight that have essentially overfunded their pension obligations. They include Estonia, Denmark, Sweden and Australia.

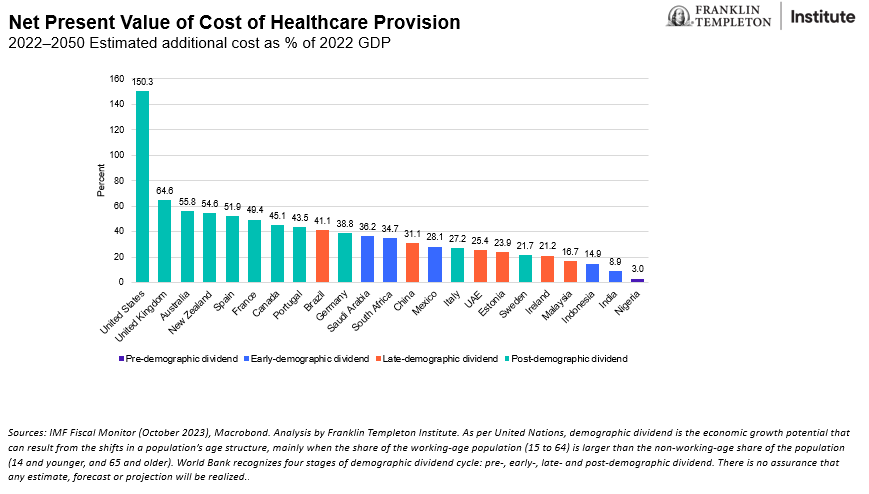

Exhibit 2: The Economic and Fiscal impact of Aging Populations

Exhibit 2 above demonstrates the difference in healthcare liabilities between, for example, Nigeria and the United States. The longer people live, the more healthcare they will typically require; therefore, the higher the cost. In the United Kingdom, an equivalent of more than 64% of 2022 GDP will be needed to cover the healthcare liabilities of 2050. In the United States, that number is 150% of 2022 GDP. The point about policy remains the most important variable, in our view. In the countries we highlight here, Sweden is the best-prepared aging country—because of historic policy action.

Conclusion

The traditional view of demographics as a driver of economic growth is no longer appropriate, in our view. Qualitative factors override this assumption. For aging countries, the challenge is primarily to ensure continuous improvement in educational standards, because their economies are becoming more knowledge- and technology-driven. For countries with more youthful demographics, the challenge is similarly education-related, because they need to offer more than cheap unit labor costs.

However, the global economic and geopolitical environment has constrained policymakers’ options, as businesses diversify supply chains and respond to incentives for investment, such as the US government’s Inflation Reduction Act. This means that high-fertility countries cannot simply follow the old playbook of attracting foreign direct investment into labor-intensive industries; they must try to leverage their mineral wealth or their strategic positioning instead.

Allowing for cultural and wealth disparities between countries, consumption patterns generally will change. This evolution of savings and investment will drive real interest rates, real exchange rates and even returns on investment. Demographics are not destiny, but can set parameters.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Investments in companies in a specific country or region may experience greater volatility than those that are more broadly diversified geographically.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

1. Source: Ninth National Workforce Survey, All-China Federation of Trade Unions; National Bureau of Statistics.

2. The United Nations Population Fund definition holds that there is a demographic dividend, i.e., a period of accelerated economic growth that may occur when a country has a growing population of workers, because they are productive generators of economic wealth.