Private equity: Secondaries anyone?

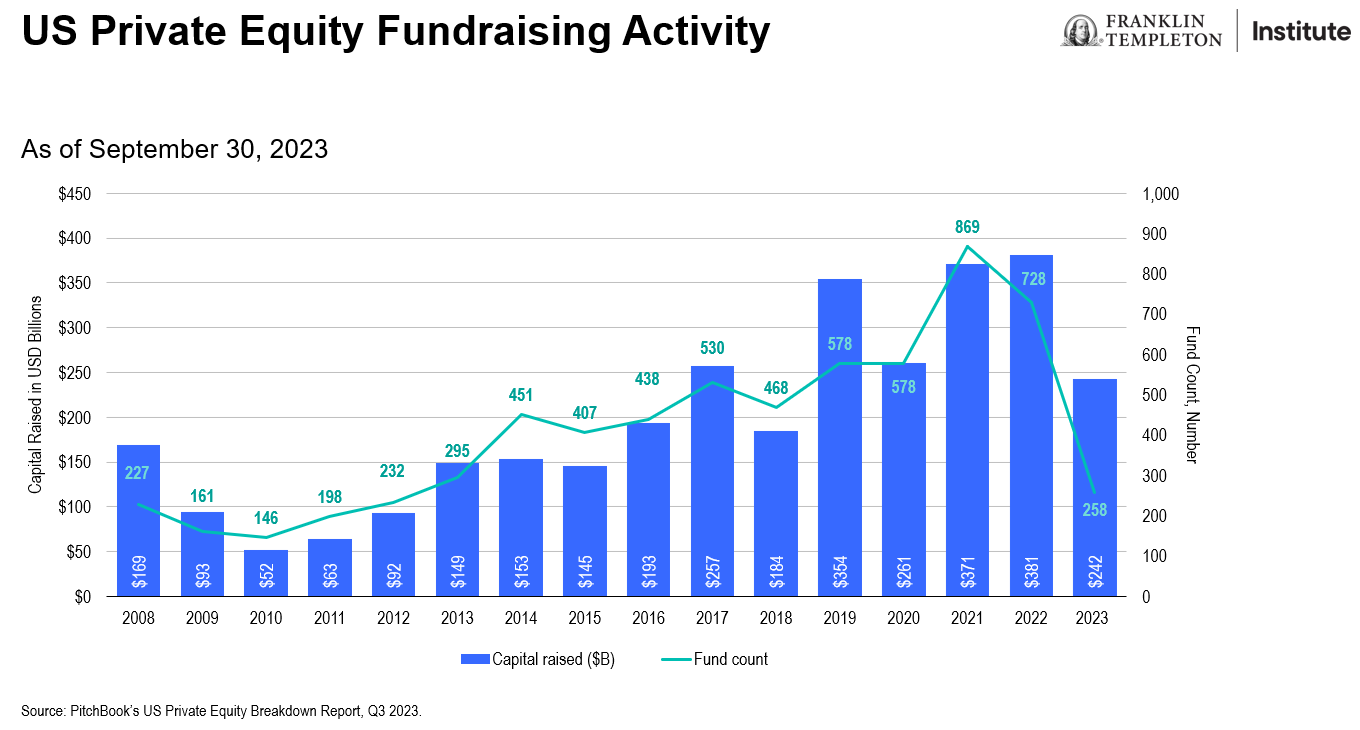

During the recent environment of easy money and growing demand, private equity (PE) fundraising grew rapidly over the last two decades. From 2011–2021, private equity generated 11 consecutive years of net distributions to limited partners (LP), meaning institutions could typically count on distributions offsetting commitments. However, as noted in our “2023 Private Market Outlook,” private equity exits slowed dramatically in 2022, and continue to be stalled as of the writing of this report.

Private equity valuations reset from their lofty 2021 valuations. Higher interest rates and tighter credit conditions should put pressure on PE valuations, and investors may need to brace for a down round. Private equity fundraising is down substantially from its 2021 peak.

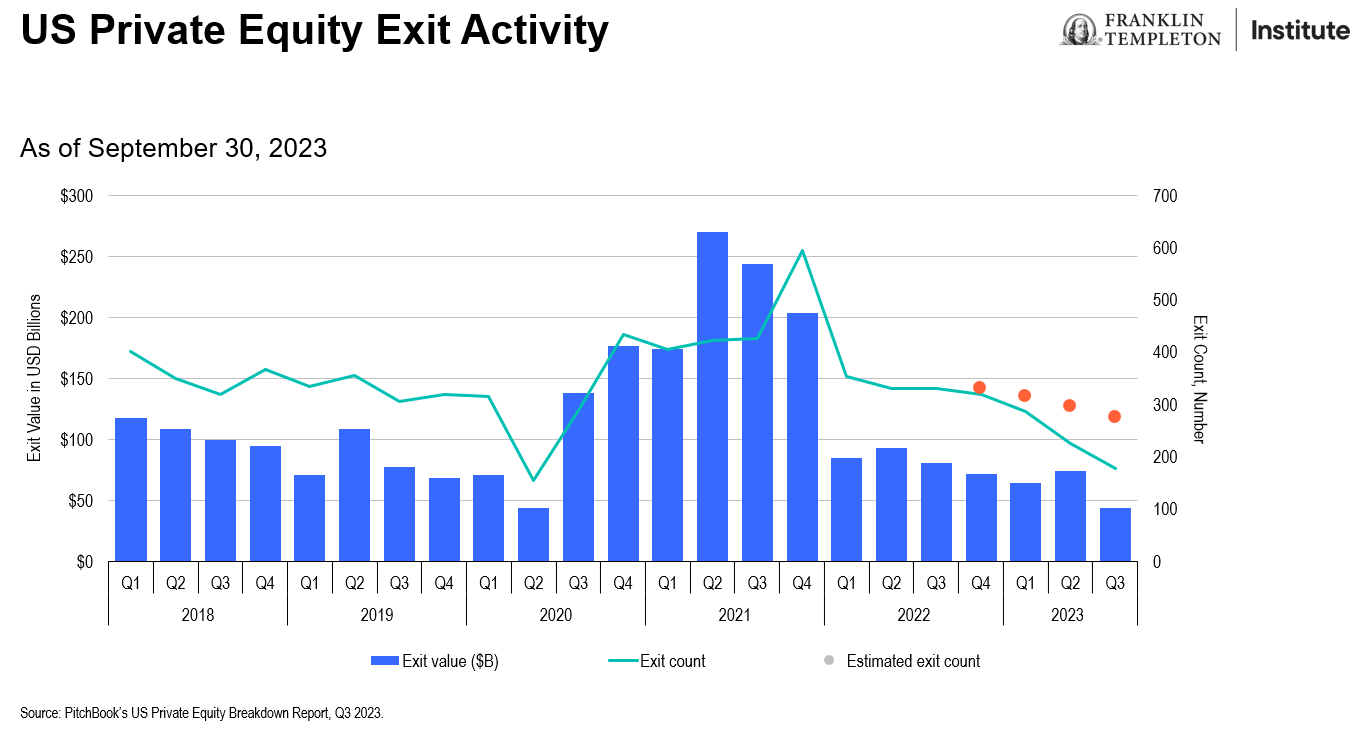

According to PitchBook,1 “Exit value hit an air pocket in Q3, falling 40.7% from the prior quarter to its lowest quarterly level since the global financial crisis—and is now down 83.7% from the Q2 2021 peak.”

Exit activity is arguably the most important link in the PE chain of capital formation and an indicator of the health of the overall PE market. Exits fuel fundraising which leads to increased dry powder and the investment of capital. Exits also impact the allocation/reallocation of capital across institutions.

Secondaries

While PE deals and exits have slowed, secondaries activity has picked up precipitously as institutional investors seek to rebalance their portfolios. Many institutions committed significant capital to PE in the last decade due to the potential for oversized returns. The expectation was they would be rewarded in the form of an illiquidity premium—the excess return for giving PE managers ample time to unlock value—and they would begin to receive distributions as investments reached the harvest period.

As institutions found themselves overallocated to PE, they sought a means to diversify their holdings and still meet future commitments by accessing the secondary market. The secondary managers have been able to select from broad pools of assets to acquire attractive investment interests at favorable pricing. The managers benefitted from the significant inventory and the institutions’ need for liquidity.

Secondaries managers can be selective in deploying capital, and can diversify across stages of development (venture capital, growth equity, and buyout), geography, industry, and vintage. By purchasing assets closer to their harvest stage, secondaries managers can mitigate the effects of the J-Curve, and investors may receive distributions sooner. Secondaries managers may also avoid troubled assets and select prized assets.

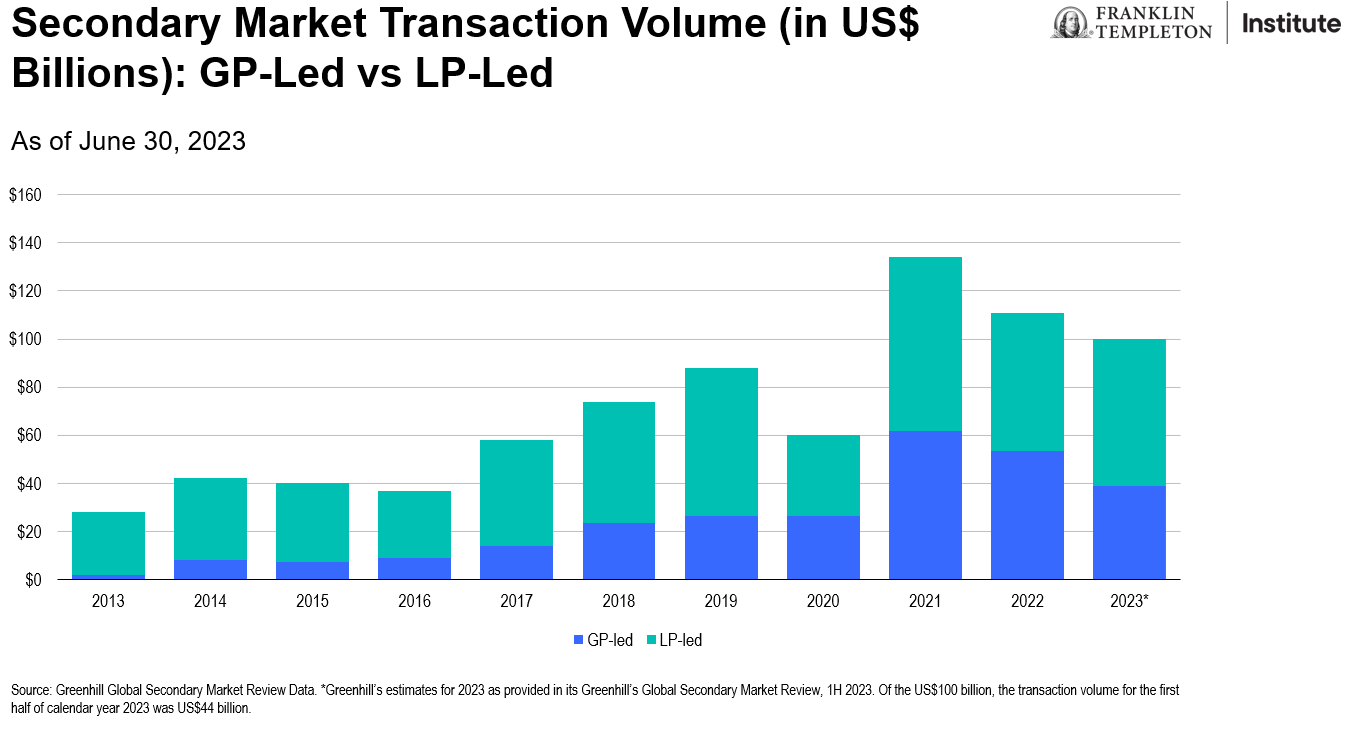

There are two types of secondaries: “LP-Led” and “general partner (GP)-Led.” In an LP-led transaction, a limited partner sells its commitment in a fund to a secondary buyer, who then takes on the rights and obligations of that LP in the existing fund. In a GP-led transaction, a GP-led single-asset continuation transaction, an asset or portfolio company is transferred from one vehicle to another vehicle, which can offer access to both additional capital and additional time to execute a value-creation plan. Within GP-led secondaries, the single-asset model now stands as a functionally distinct segment, and single-asset transactions are the fastest-growing area within secondaries. GP-led single-asset secondaries can offer attractive benefits in all market conditions because of the flexibility for GPs to hold their most promising assets longer, and the possibility of added exit options.

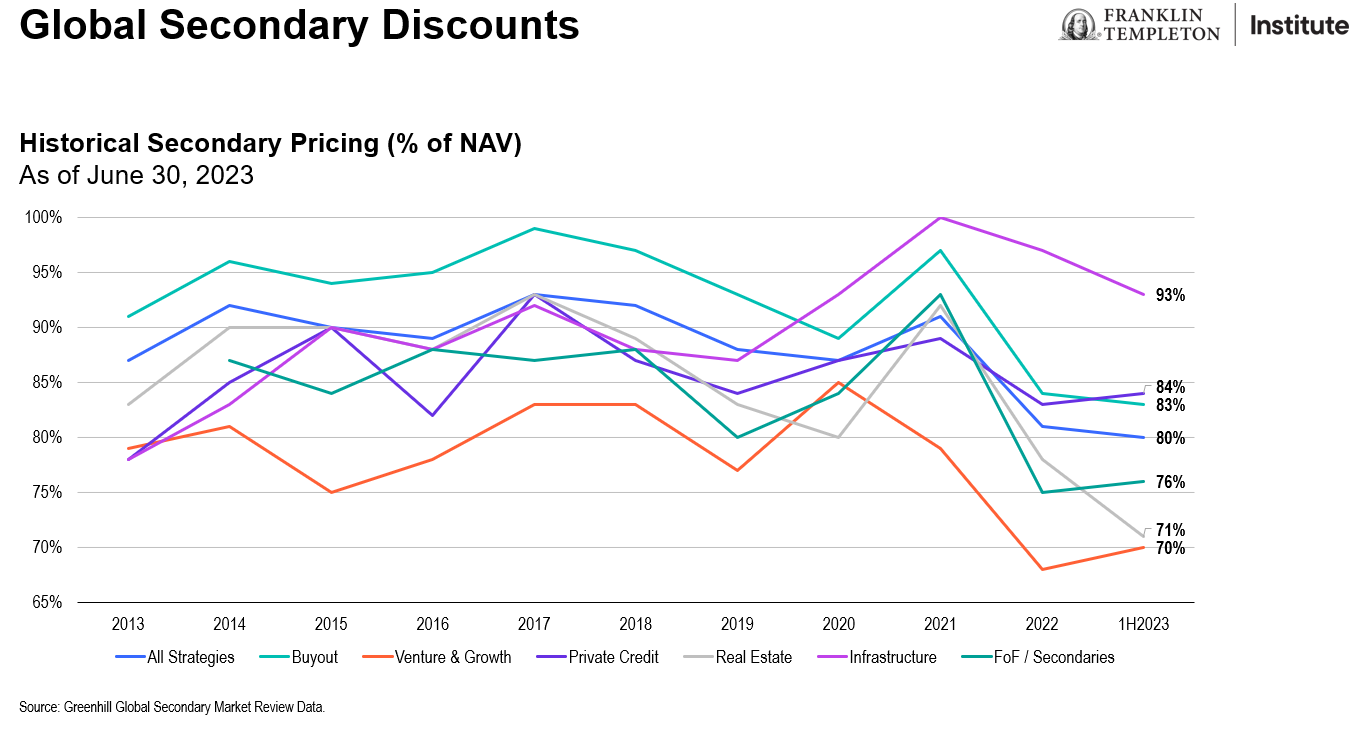

Secondaries valuations

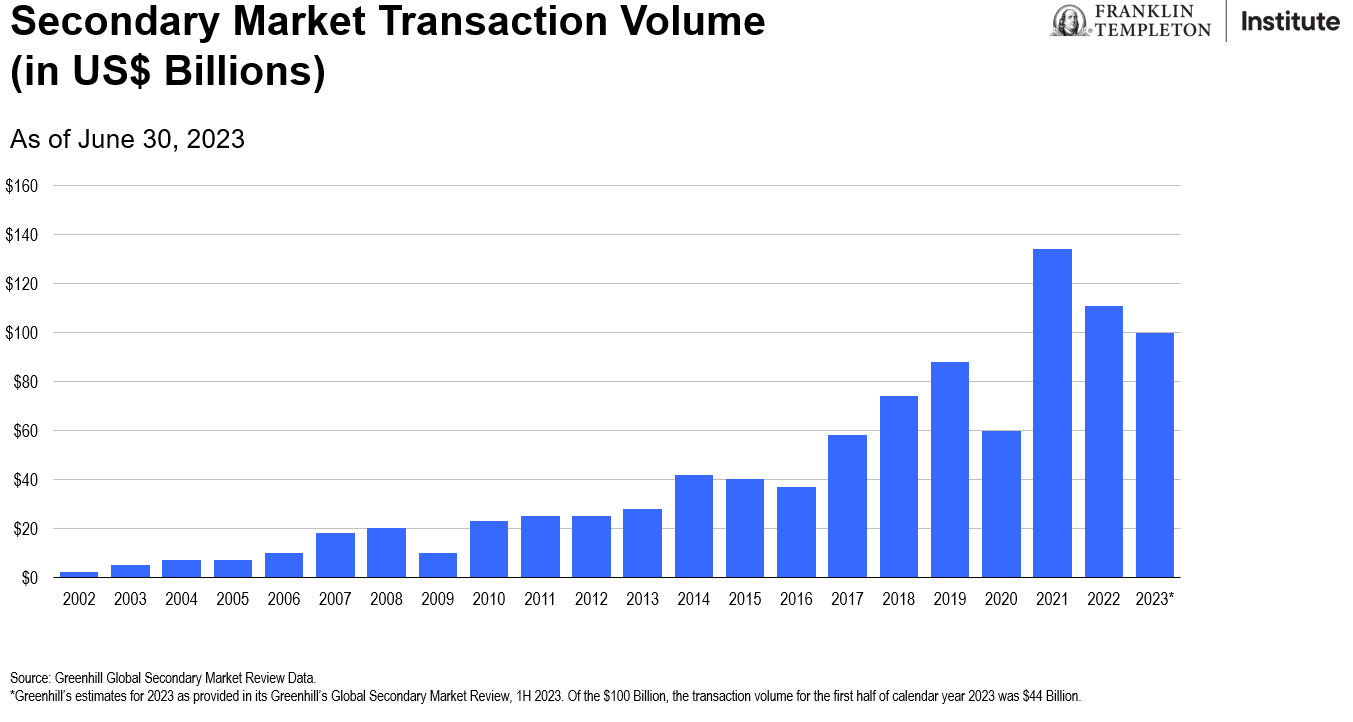

The secondaries market has grown substantially over the last decade, from US$20 billion in 2006, to US$134 billion in 2021.2 As the market has matured, more sellers access the market which has led to increased deal flow and LP portfolios are generally available at a discount to the underlying valuation.

It is important to note that pricing varies across the private markets, with significant differences between venture and buyout valuations. According to Greenhill,3 the average pricing for LP transactions rebounded to 80% of net asset value (NAV), with venture pricing at 70% and buyouts 83%, reflecting the divergence across the private-market ecosystem.

During 2022 and 2023, we saw increasing discounts as compared to the stable price environment of prior years, driven by the recent market volatility and an expectation for declining NAVs, which have resulted in more conservative underwriting by secondary buyers, which typically drives discounts wider. Investors are increasingly seeking liquidity as portfolio distributions decline, which drives increased volume. The elevated volume of portfolio sales comes as secondary industry dry powder dries up. We anticipate a period of higher average discounts will continue until NAVs stabilize for multiple successive quarters.

Secondaries have become a vital cog in the growing private equity ecosystem, providing investors with access to liquidity. Secondaries provide diversification and provide the broader ecosystem with additional scale and liquidity during periods of stalled exits.

Venture capital

According to Pitchbook,4 “Venture-growth-stage startups face the harsh reality that median deal metrics have fallen more than 60% from record highs in recent years. The prolonged lack of liquidity and pullback of nontraditional investors have provided active investors ample leverage to demand higher equity stakes, with the 2023 YTD median notching a decade high of 14.9%.” There has been a significant change in the market environment over the past 12 months, which has impacted valuations and capital formation within these innovative areas.

With respect to venture capital, we see a big difference between committed capital and new capital. Committed capital is dependent on when capital was committed, and at what valuation. Unfortunately, capital committed over the last couple of years is likely held at lofty valuations and may be dramatically different than the current valuation.

Conversely, managers putting capital to work today can be more selective in the investments they make, and the valuation of those investments. This could represent an attractive entry point for new VC capital.

Takeaways

Private equity valuations are being reset from their 2021 levels and exits have slowed to a crawl. Coming out of 2022, many institutions found themselves overallocated to PE, and/or unable to meet future commitments. Many sought to meet their allocation and liquidity needs by selling to secondary managers.

The private equity ecosystem represents a diverse set of opportunities from venture to growth to buyout, and provides diversified exposure across industry, across geography, and vintage year. Secondaries represent an attractive and growing opportunity to access this ecosystem.

To learn more please visit AltsbyFT Knowledge Hub. Knowledge Hub | Alternatives by FT.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Investments in many alternative investment strategies are complex and speculative, entail significant risk and should not be considered a complete investment program. Depending on the product invested in, an investment in alternative strategies may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. An investment strategy focused primarily on privately held companies presents certain challenges and involves incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity. Diversification does not guarantee a profit or protect against a loss.

Risks of investing in real estate investments include but are not limited to fluctuations in lease occupancy rates and operating expenses, variations in rental schedules, which in turn may be adversely affected by local, state, national or international economic conditions. Such conditions may be impacted by the supply and demand for real estate properties, zoning laws, rent control laws, real property taxes, the availability and costs of financing, and environmental laws. Furthermore, investments in real estate are also impacted by market disruptions caused by regional concerns, political upheaval, sovereign debt crises, and uninsured losses (generally from catastrophic events such as earthquakes, floods and wars). Investments in real estate related securities, such as asset-backed or mortgage-backed securities are subject to prepayment and extension risks.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

An investment in private securities (such as private equity or private credit) or vehicles which invest in them, should be viewed as illiquid and may require a long-term commitment with no certainty of return. The value of and return on such investments will vary due to, among other things, changes in market rates of interest, general economic conditions, economic conditions in particular industries, the condition of financial markets and the financial condition of the issuers of the investments. There also can be no assurance that companies will list their securities on a securities exchange, as such, the lack of an established, liquid secondary market for some investments may have an adverse effect on the market value of those investments and on an investor’s ability to dispose of them at a favorable time or price. Past performance does not guarantee future results.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Copyright © 2024 Franklin Templeton. All rights reserved.

_______________________________

1. Source: PitchBook. “PE Breakdown.” October 2023.

2. Source: Collum, Chase. “Six key trends shaping the secondaries market.” Buyouts Insider web site. June 1, 2022.

3. Source: Pitchbook. “US VC Valuations Report.” November 8, 2023.

4. Ibid.