Japan may be blossoming again. Goods and wage inflation are returning, some companies are embracing real and significant corporate reforms, the equity market has surged, and foreign investors are showing sustained enthusiasm. Nonetheless, we believe investors in the Japanese market still need to be selective when searching for companies that can unlock value as not every firm is fully, or enthusiastically, warming to change.

Goods-and-wage inflation flower

The Japanese economy appears to us to be emerging from years of stagnation. We believe a rebound in inflation in both goods and wages should help the country boost economic dynamism and spark a period of hotter and more sustained growth.

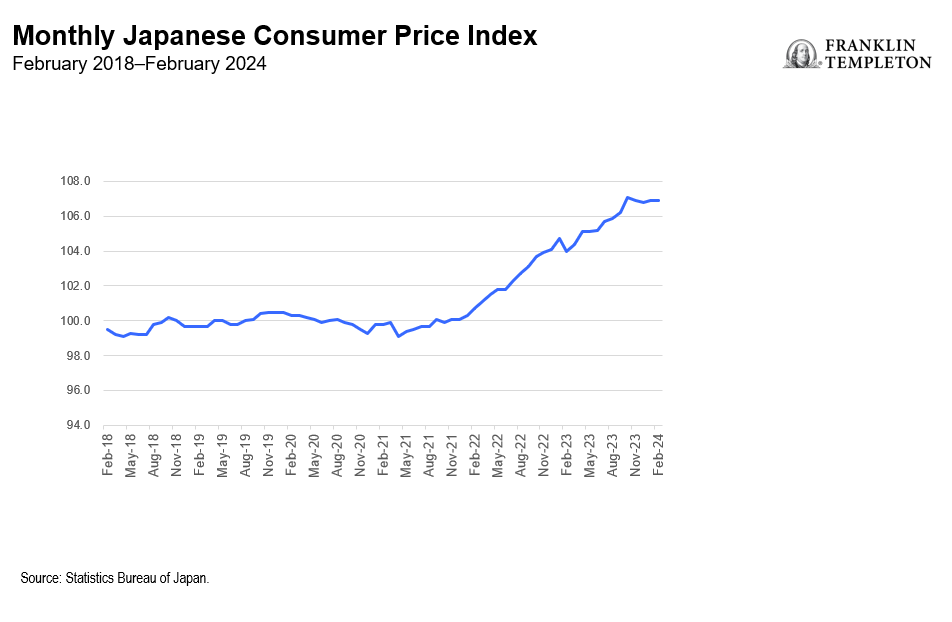

Corporate Japan has shown a greater willingness and ability to raise prices and overall inflation is now approaching the Bank of Japan’s (BoJ’s) 2% target. (See Exhibit 1).

Exhibit 1: Monthly Japanese Consumer Price Index Climbs

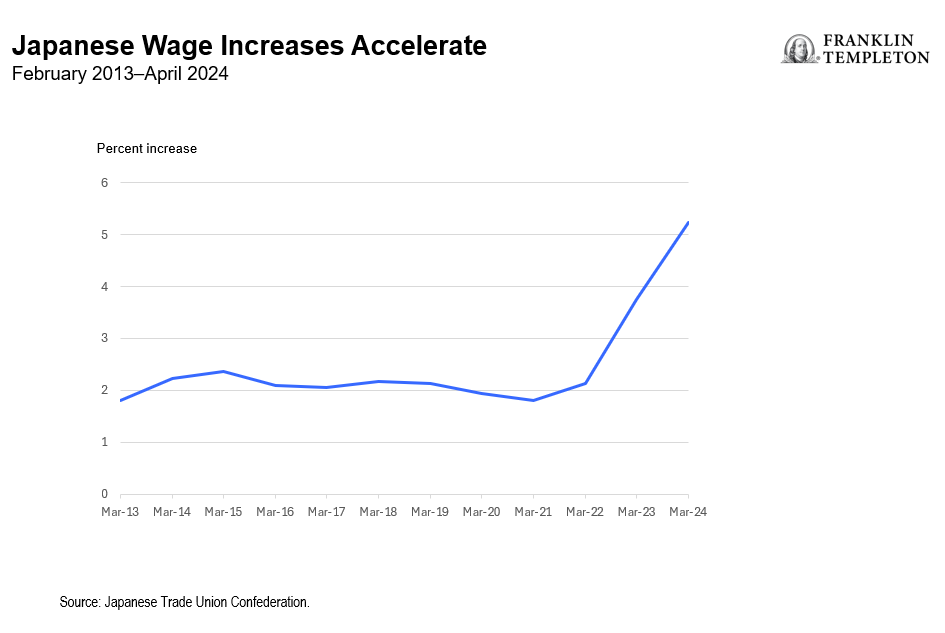

Wage growth, which has lagged price increases, is also starting to climb as companies need to pay their employees more to afford costlier goods. The spring labor negotiations suggest a significant wage hike for Japanese workers in the coming year. Labor unions secured a 5.24% average total wage hike through three rounds of negotiations, up from an average wage increase of 3.6% in 2023, according to Rengo, the Japanese Trade Union Confederation. (See Exhibit 2).

Wage growth, which has lagged price increases, is also starting to climb as companies need to pay their employees more to afford costlier goods. The spring labor negotiations suggest a significant wage hike for Japanese workers in the coming year. Labor unions secured a 5.24% average total wage hike through three rounds of negotiations, up from an average wage increase of 3.6% in 2023, according to Rengo, the Japanese Trade Union Confederation. (See Exhibit 2).

Exhibit 2: Japanese Wage Increases Accelerate

Crucially, we believe higher wages can help end the negative spiral of falling prices and stagnant wages the economy has been in over the past few decades and move it to a place where inflation is expected to be structurally sustained at positive levels. Dynamism could return to the Japanese economy as a result.

Interest rates begin to bud

With inflation in both goods and wages picking up, the BoJ ended decades of experimental monetary policy and negative interest rates in late March.1 For the first time since 2007, it raised rates to a 0-0.1% range. The central bank also reduced quantitative easing measures.

While we view this move as a small step, we believe the BoJ will continue to gradually normalize monetary policy over the next couple of years. If it turns out that the economy starts to improve, wages rise and modest inflation remains a regular occurrence, then we would expect the BoJ to take additional steps to tighten monetary policy.

Corporate reforms bloom

At the same time the economy is improving, corporate Japan is beginning to embrace change, spurred on by the Tokyo Stock Exchange (TSE). The TSE is encouraging companies to improve their returns and reduce their cost of capital as part of a push to make the country more investable. Furthermore, new rules will push companies to simultaneously release earnings and other disclosures in English, making the market more appealing to overseas, non-Japanese speaking investors.

While the exchange has had a good initial response from most large-cap companies in laying out their plans, smaller companies have not been as forthcoming, in our view. The Tokyo Stock Exchange expects to keep pushing companies that have not fully put forward plans to reduce their cost of capital to eventually do so. We are naturally more interested in the companies that have realistic plans which, if successful, we expect can drive tremendous long-term returns for shareholders.

There is much work to do in Japan as a third of companies have price-to-book ratios below one and low returns on equity. Of the 4,015 active stocks on the Tokyo Stock Exchange at the end of March, about 39% have price-to-book values below one, while 34% of companies have a return on equity of less than 5%, according to data from FactSet.

The TSE and the Japanese government are also pushing companies to reduce their cross-shareholdings, which are widely seen as a barrier to market efficiency and transparency, as well as a barrier to mergers and acquisitions. These holdings have been common in Japan for decades, as companies held stock in their customers and vice versa to cement and maintain business relationships. While this system has worked for the individual Japanese companies themselves, it has not typically worked for anyone else, including investors.

We have seen some companies unwind their holdings while others have just begun to consider their own plans. Although the changes have been slow, as more companies make real progress on this front, we would expect momentum to continue to build until real change blooms.

While reducing cross-shareholdings is a positive, we want to see what companies do with the cash from these sales. Those firms that want to buy growth at home or overseas look less appealing to us on first blush, given Japanese companies’ poor record of overseas acquisitions, than those that may return cash to shareholders through stock buybacks or fatter dividends.

Blossoming value stock opportunities

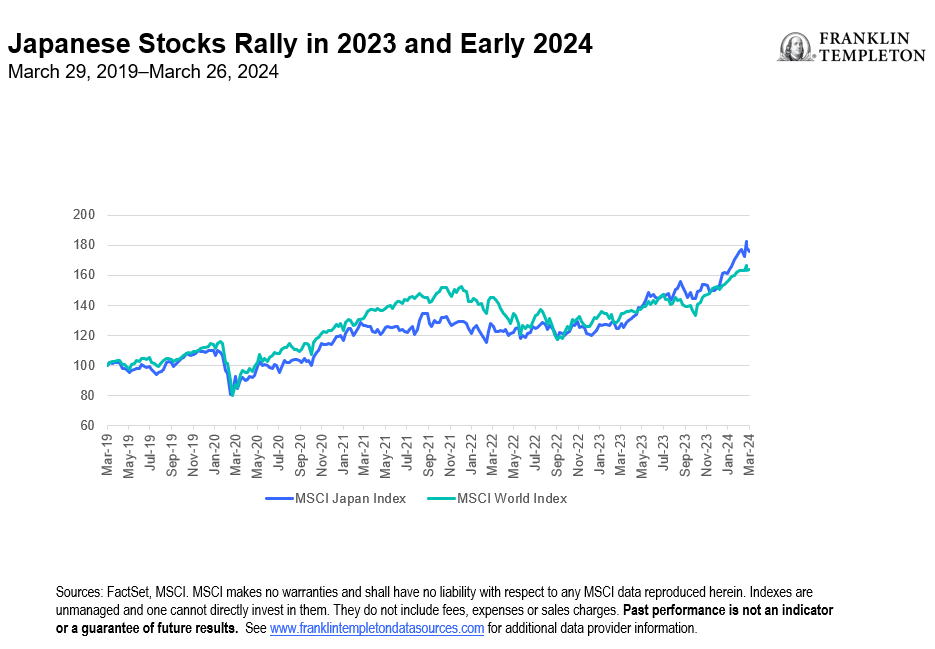

Enthusiasm about these corporate and economic changes in Japan has spilled over into the equity market, with the MSCI Japan rising sharply since the start of 2023 (see Exhibit 3). While we believe enthusiasm for Japan is justified, finding compelling value opportunities after the runup will require careful stock selection.

Exhibit 3: Japanese Stocks Rally in 2023 and Early 2024

We believe companies that have a clear plan to improve their returns and reduce their cost of capital, and that are willing to buy back stock trading below book following the unwinding of cross-shareholdings, are more appealing than those that are simply posturing. Additionally, companies that are managing toward a medium-term growth plan and capital allocation strategy can be better judged on their success.

In our view, the companies that are successful could see a significant runway for growth and potential stock price appreciation as book values improve over the medium term. This burgeoning Japanese spring could turn into a long summer.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.. Active management does not ensure gains or protect against market declines.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

_____________

1. Source: Bank of Japan, March 19, 2024.