To find and retain talent, employers continue to broaden their benefits programs. But employers’ offerings may not be in sync with what workers want.

Franklin Templeton’s 2024 “Voice of the American Workplace” survey found most workers are seeking more financial benefits. Being financially independent is a leading goal and financial benefits, such as an increase in salary or larger 401(k) match, are easily quantified.

At the same time, many employers focus on offering improved health benefits and financial wellness programs. While health care is an important consideration, employees don’t always understand the value of some benefits, resulting in an underutilization of programs. This could also impact their retirement planning and financial security.

The VOTAW survey found 70% of employer plan sponsors have increased the number and quality of their benefits in recent years. At the same time, 72% of employees reported some type of challenge in understanding the offerings. For example, responding to growing demand, 49% of employers introduced financial wellness programs, but only 28% of employees said they took advantage of them.

To achieve the most participation and deliver valued benefits, employers want to know what workers are seeking, and how best to communicate the offerings.

How employees choose benefits may offer insights

Many employers surveyed (85%) said employees have increasingly asked about personalized benefits. The data suggest more choice and flexibility could boost engagement and may influence employee decision-making about their jobs.

In addition, 63% of employers noted that voluntary benefits have become increasingly popular among their workforce.

Work-life balance gains traction

The personalization of benefits is a growing trend. It emerged in response to changes in the healthcare system allowing for more options and the changing workplace, which is providing more hybrid and remote work flexibility.

Work-life balance has been a growing focus of employees and employers, particularly since the COVID-19 pandemic. Most employers surveyed (87%) said: “Hybrid or remote work supports employee well-being, reducing stress related to commuting and enabling a healthier work-life balance,” with 85% admitting that it’s also an effective recruiting and retention tool.

In the area of healthcare, many companies offer a choice in plans. Today’s workers may find an array of health plans with varying degrees of coverage and deductibles. Some plans, such as high-deductible health plans, also allow participants to save in health savings accounts (HSAs), which offer multiple tax advantages and may support long-term financial goals.

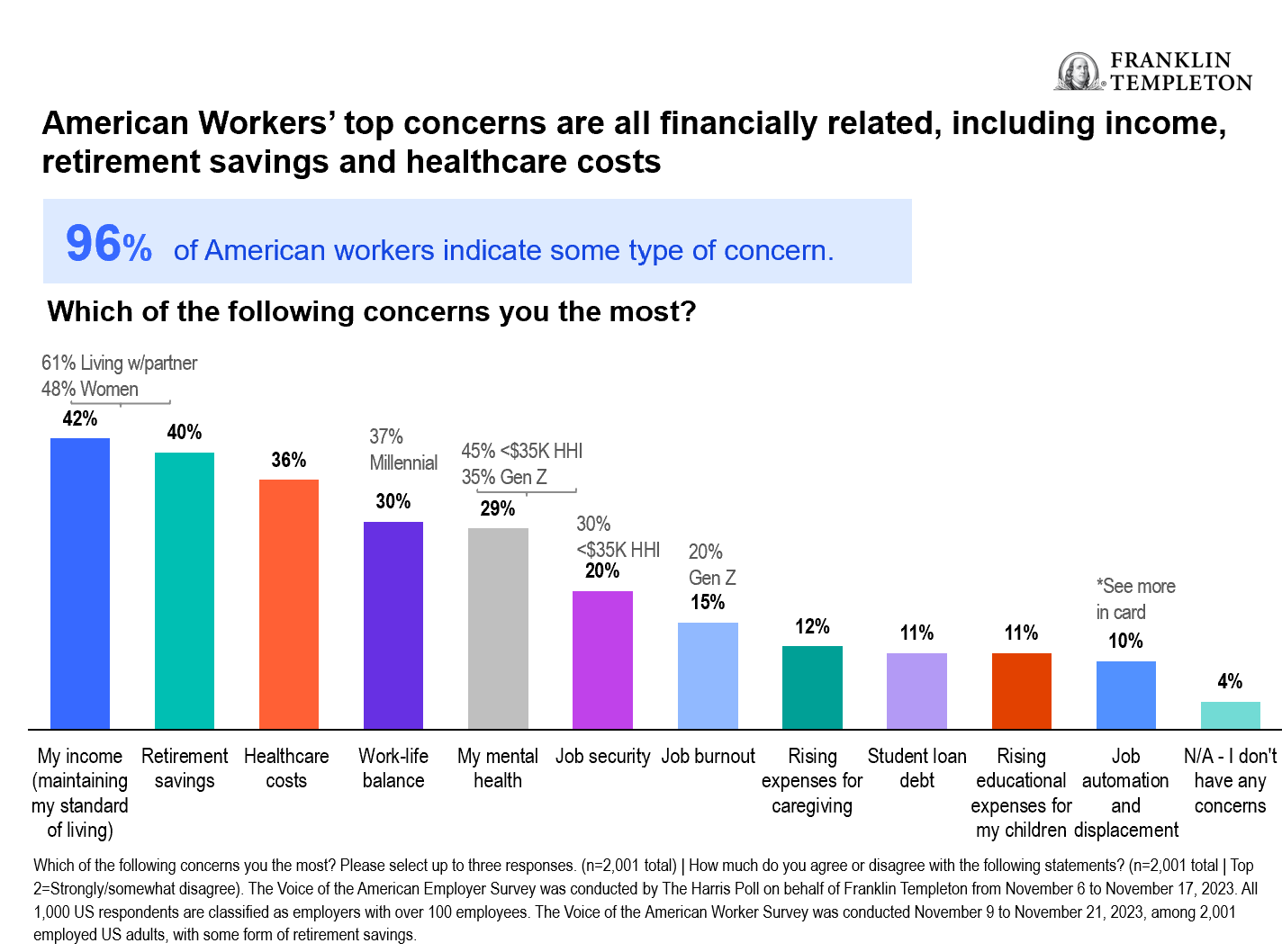

Workers are concerned about finances

Workers’ concerns are largely related to finances, including income, retirement savings and healthcare costs. Within retirement savings benefits, workers want more choices and personalization of their 401(k) plans. Nearly two-thirds (59%) are worried about running out of money in retirement and 55% plan to do some work in retirement.

According to our survey, workers want to save, but they want to have a plan that suits their individual financial goals.

(right click to enlarge/open in new window)

Workplace savings offer opportunity for personalization

Workplace retirement savings plans offer opportunities to present workers with the flexibility to customize their savings to meet multiple goals.

(right click to enlarge/open in new window)

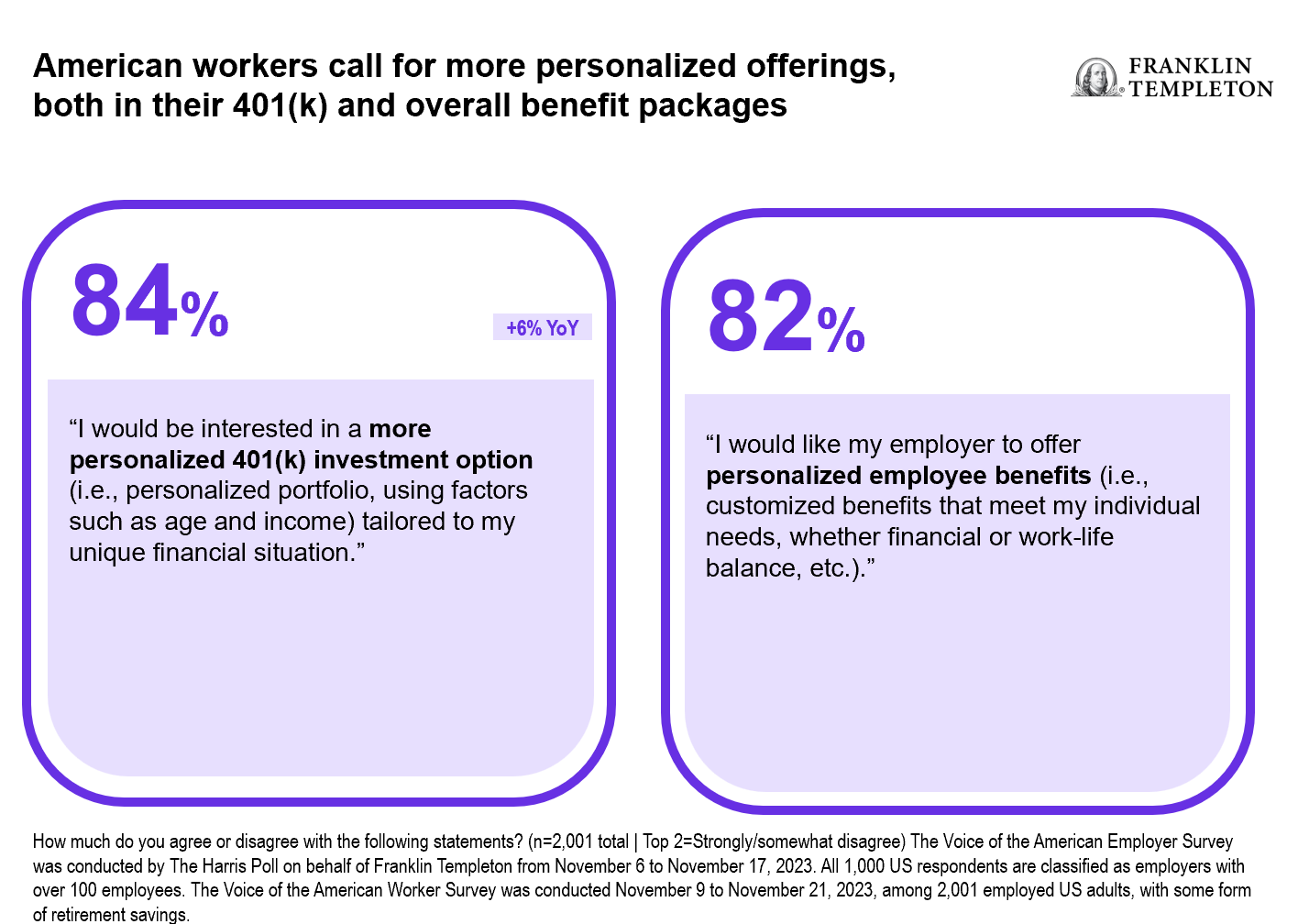

The survey found 84% would be interested in a more personalized 401(k) investment option such as “a personalized portfolio, using factors such as age and income tailored to my unique financial situation.”

Also, 82% of workers surveyed said they would like to see customized benefits to meet their individual needs including financial and work-life balance goals.

Target-date strategies, a common default option in most 401(k) plans, have grown in popularity as a one-stop solution for retirement savers. The next generation of this strategy also focuses on greater personalization. A growing number of employers are considering more tailored investment strategies that are customized for a participant’s income, time horizon and individual savings goals within defined contribution plans.

Workers also recognize the value of the employer match in a 401(k) plan and 42% said they would like to see a larger match.

How the employer match is distributed is another area that is changing

The SECURE 2.0 legislation allows employers to use a company match to help participants as they make student loan payments. In fact, many workers (84%) surveyed said they are interested in student loan repayment assistance.

Today, student debt in the United States totals more than $1.7 trillion,1 and it is easy to understand how debt can be an obstacle to saving. Several studies found that workers with student loan debt on average contribute less to their workplace retirement plans compared with workers without debt. In our study, 47% of Millennial workers said, “Student loan debt is holding me back from significant financial milestones like buying a home or saving for retirement.”

Student loan assistance may help attract workers as well as support their savings goals.

Additional 401(k) options

Other policy changes allow employers to include a Roth option within their 401(k) plans, enabling participants to diversify their investments from a tax perspective. Some plan designs also help workers accumulate emergency savings.

Boosting engagement

The evolution of the 529 college savings plan is another example of how increased flexibility can engage more individuals. Originally designed to help families save for college, recent policy changes have expanded the use of 529 plans. In addition, 529 plans may be used for K-12 education tuition, qualified apprenticeship programs, funding of ABLE Accounts for people with disabilities, and student loan payment assistance. As of 2024, unused 529 assets may also be rolled over into a Roth IRA (within limits).

Our VOTAW study found as awareness of 529 plans grows, two-thirds of workers surveyed said they would be inclined to open an account knowing it can be used for more than college expenses.

New 529 account openings have grown steadily, reaching 15.9 million in 2022 from 10 million in 2009. Assets have also grown to $412.5 billion in 2022 from $133 billion in 2009, according to the College Savings Plans Network.2

Holistic approach to benefits

In general, workers want to see more choice in benefits that can be customized to meet their financial or work-life goals. With recent policy changes, there are a growing number of opportunities to create more choices and personalization in 401(k) plans. This valued retirement savings option may be able to help participants meet many of their goals.

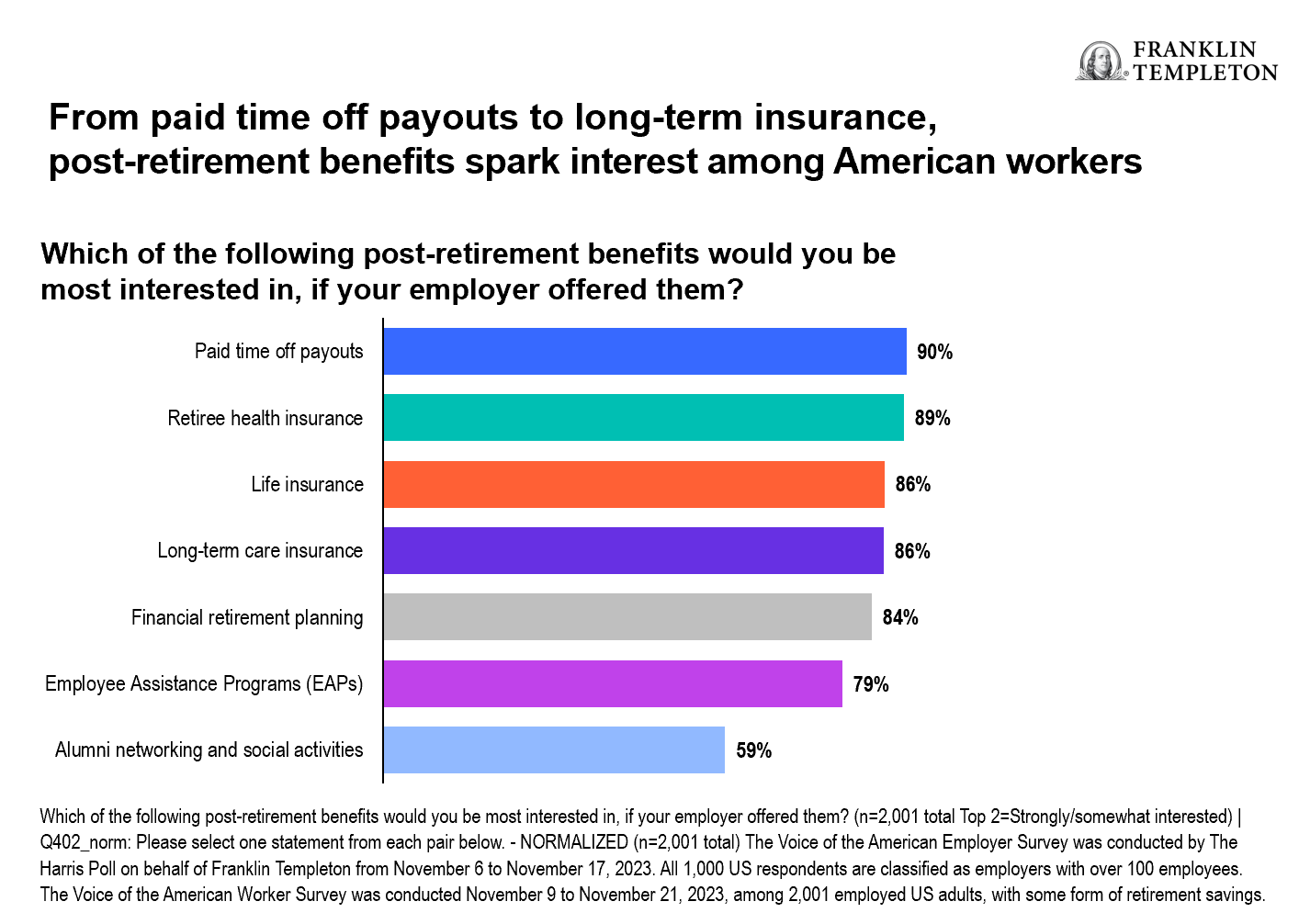

The survey also found workers are focused on benefits that support financial independence. Consider the interest in offerings that will take them into retirement.

(right click to enlarge/open in new window)

For additional information, please contact the Franklin Templeton Retirement Sales Department at (800) 530-2432.

The Voice of the American Employer Survey was conducted by The Harris Poll on behalf of Franklin Templeton from November 6th to November 17th, 2023. All 1,000 respondents, based in the United States, are classified as employers, defined as having at least some influence over company benefits and/or hiring at organizations with over 100 employees. Respondents represent a mix of industries, company size, role, age, and race.

This presentation also references a qualitative study conducted by The Harris Poll on behalf of Franklin Templeton from August 15th to August 25th, 2023, among 15 American employers. All interviewees were full-time employees working in human resources, who have influence over employee benefits, and included those with titles such as HR Manager, HR Director or HR Vice President, among others.

This was a blind study, as Franklin Templeton was not mentioned in order to avoid bias.

The Voice of the American Worker Survey was conducted by The Harris Poll on behalf of Franklin Templeton from November 9th to November 21st, 2023, among 2,001 employed US adults. All respondents had some form of retirement savings. This online survey is not based on a probability sample and therefore no estimate of theoretical sampling error can be calculated. Findings from 2020 reference a study of a similar nature that was conducted by The Harris Poll on behalf of Franklin Templeton from October 16 to 28, 2020, among 1,007 employed US adults, study from 2021 also references a similar survey conducted among 1,005 employed adults from October 28th to November 15th, and a study from 2022 also references a similar survey conducted among 1,000 employed adults from October 17th to October 27th.

Franklin Templeton is not affiliated with The Harris Poll, Harris Insights & Analytics, a Stagwell LLC Company.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Copyright © 2024 Franklin Templeton. All rights reserved.

1Source: Education Data Initiative, data as of 2023.

2Source: College Savings Plans Network, data as of 2022.