The sun is setting over 10 Downing Street

Broad measures of UK equity performance like the FTSE UK RIC Capped Net Tax Index have have posted record levels in the wake of local elections.1 The last on-the-ground test of political sentiment in the country before the general election only confirmed what polls have been predicting for a while now: Prime Minister Rishi Sunak’s Conservative Party is heading for a crushing defeat, some five years after winning a historic majority. When former Prime Minister Boris Johnson pushed through a snap election at the end of 2019, his promise to “get Brexit done” carried the Tories to the largest Conservative majority since Margaret Thatcher. Of course, a few COVID lockdown parties and poor staff choices later, “Bojo” was forced to step down and Liz Truss took over. Lasting just 50 days, her premiership was the second-shortest since 1721, the year that Sir Robert Walpole become the country’s first de-facto prime minister.2 While Rishi Sunak’s tenure has been free from major scandals, after 14 years of Tory rule, the country seems to be yearning for change.

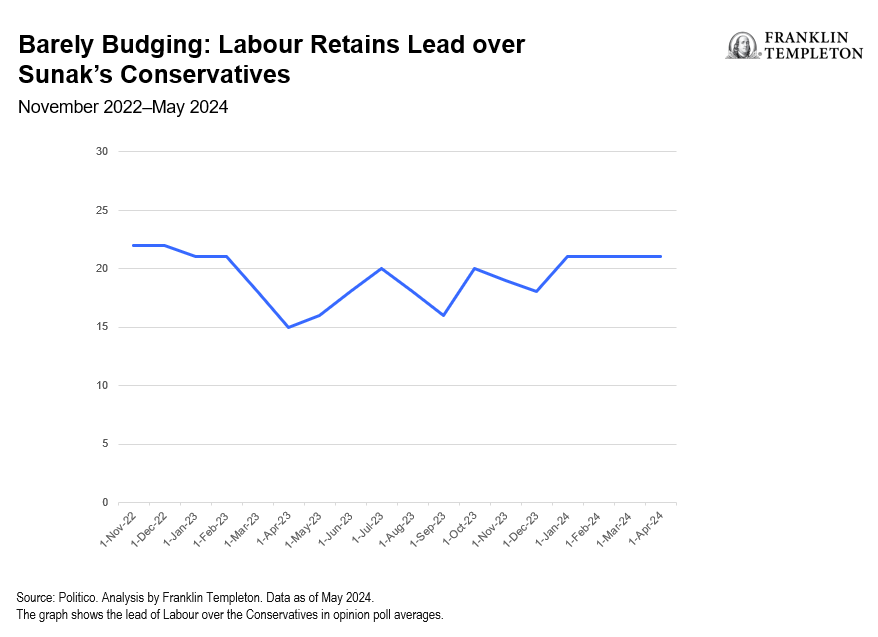

The Labour Party maintains a huge lead in the polls of around 20 points, or 44%,3 leaving chances of another Tory majority unlikely. Given that the government has some flexibility in setting the general election, Sunak’s best bet could be to push the date back as far as possible—in this case, January 2025. This would allow more time for some of his key pledges to materialize, namely taming inflation, stopping illegal immigration across the English Channel and cutting National Health Service (NHS) waiting times.4

Ultimately, however, the prime minister appears to be left with no good options.

Economic policy differences may play out at the margins

The question is whether any of these considerations matter to the markets. We think that more likely than not, we believe the upcoming campaign and election outcome will be of limited significance. Compared to the United States, policy differences between the main parties remain moderate. The political turmoil around Brexit has mostly settled, and the issue has lost much of its ideologically divisive power. Labour might try to foster stronger trade relations with the European Union (EU) but finds itself similarly constrained by the rules Brussels has set. Labour leaders have said that there are no plans to hike income taxes;5 Conservatives are pushing for lower taxes, but economic realities dictate that any cuts would have to be marginal. Energy giants might face a more structured approach to windfall taxes, but in practice, Tory governments had implemented these levies on at least three occasions since the days of Margaret Thatcher.6 In summary, while there are obvious policy differences, their economic impact may play out at the margins.

Most likely, markets have already at least partially priced in a Labour win. Either way, the United Kingdom is in dire need of economic growth.

Diversification benefits at attractive valuations

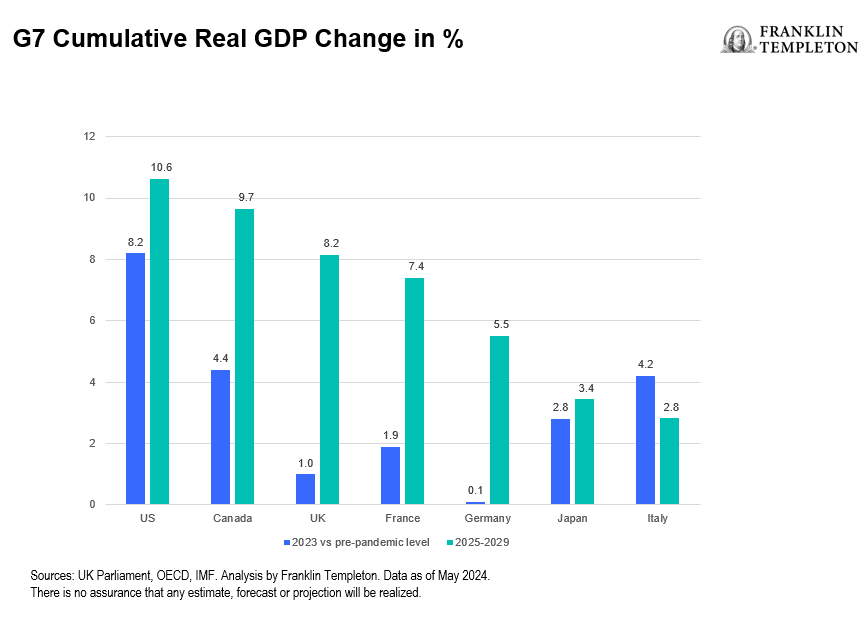

Both Brexit and the pandemic have had a disproportionate impact on the country’s economic trajectory compared to its G7 peers. In real terms, the UK economy today is only 1% larger than its pre-pandemic level. With the exception of Germany, which has experienced virtually zero growth, this is the weakest performance among its G7 peers. By contrast, the United States has seen an increase of more than 8%, while Canada and Italy have each grown by roughly 4%.

The current year is also shaping up to show lackluster growth, placing the country near the bottom of the range. However, looking ahead, the International Monetary Fund predicts that the United Kingdom will grow closer to its long-run potential, at an annual rate of between 1.5% and 2%, and is expected to add a cumulative 8% to its gross domestic product (GDP) between 2025 and 2029.7 This would position the country at the higher end of the G7 growth spectrum. Investors seeking to add targeted allocation to the UK market may find single country exchange-traded funds to be a cost-effective vehicle for exposure.

It is also noteworthy that core exposures to UK equities are only partially at the mercy of domestic economic performance. The FTSE UK RIC Capped Net Tax Index comprises large- and mid-cap stocks, including some of the top financial institutions, global players in consumer goods, and two of the world’s largest energy companies. Since 2020, it has outperformed the more domestically oriented FTSE 250 Index by almost 25 percentage points. Meanwhile, it has significantly lagged other large-cap indices, like the S&P 500 or the global FTSE Developed Index. But in times of the “Magnificent Overconcentration” of a handful of stocks and the IT sector, we think that UK equities can offer an interesting complement to investor allocations. Besides the diversification angle, there is also a valuation argument.

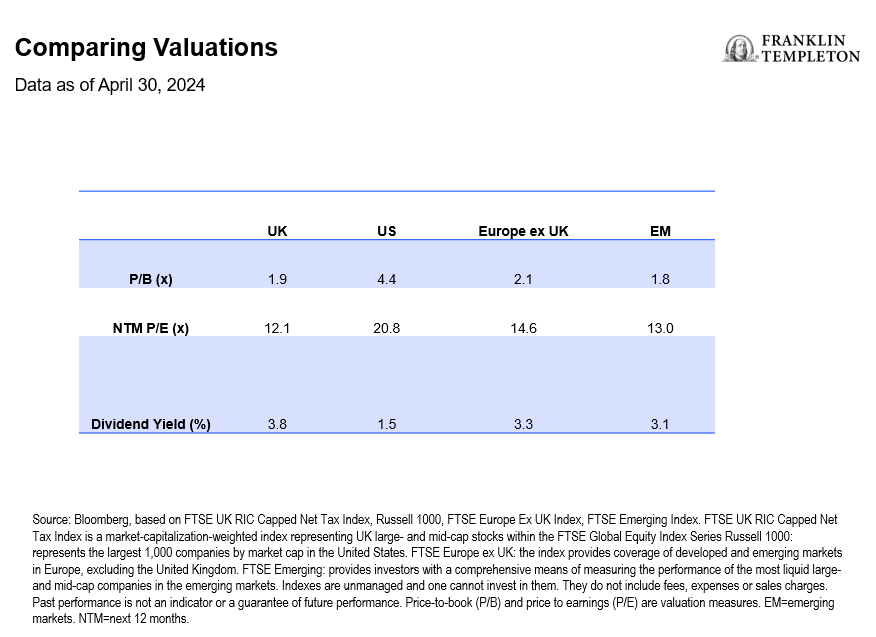

With a price-to-book ratio of less than 2.0, UK equities are currently trading at a discount of more than 50% compared to US equities. Additionally, in terms of forward price-to-earnings, they are closely aligned with emerging market levels. Furthermore, the United Kingdom has long been considered a haven for income investors, and it currently boasts a dividend yield of 3.8%.8

With the market at fresh all-time highs, investor sentiment also appears positive, but far from euphoric. The country is just coming out of the toughest cost-of-living squeeze in generations, public finances remain stretched, and the housing market is only beginning to recover.9 The Bank of England has no clear path to lower interest rates yet, although expectations for a summer cut are ramping up.

While profit-taking or election uncertainty might inject short-term volatility, we like the general setup for UK equities. A diversified exposure across sectors, a blend of global players and more local enterprises, coupled with an improving growth outlook and attractive valuations make for a compelling investment proposition, in our view.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal. International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility.

To the extent the portfolio invests in a concentration of certain securities, regions or industries, it is subject to increased volatility.

Dividends may fluctuate and are not guaranteed, and a company may reduce or eliminate its dividend at any time.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

___________________________________

1. Source: Bloomberg. FTSE UK RIC Capped Net Tax Index is a market-cap-weighted index representing UK large- and mid-cap stocks within the FTSE Global Equity Index Series. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

2. Since the office of the prime minister of the United Kingdom is established by convention rather than law, pinpointing the exact start of the first premiership is challenging. However, historians widely regard Walpole as both the first and longest-serving prime minister.

3. Source: Politico Poll of Polls. Analysis by Franklin Templeton. May 2024.

4. Source: UK Government, 2023.

5. Source: “Labour’s tax plans.” Simmons & Simmons. 2024.

6. Source: “The history of windfall taxes: who used them and why.” The Guardian. 2022.

7. Sources: Bloomberg, FTSE. 2024. There is no assurance that any estimate, forecast or projection will be realized.

8. Source: Bloomberg, FTSE, 2024. As of May 2024. Dividends may fluctuate and are not guaranteed, and a company may reduce or eliminate its dividend at any time.

9. Note: In March, mortgage approvals rose for six straight months, to the highest since September 2022. Source: Bloomberg. 2024.