Coming out of a transformative event such as the COVID-19 pandemic, people may look for a “new normal.” At the same time, the pace of change we all face may lead to a series of “next normals” vs. a singular new normal. In this article, we consider: What will the series of next normals be for the retirement plan industry?

The needs of plan sponsors and savers are changing, and that means advisors may want to view their services differently, too. A next normal value proposition needs to look beyond the “three Fs” of funds, fees and fiduciary to include customized plan design and robust client engagement.

Enhancing retirement readiness

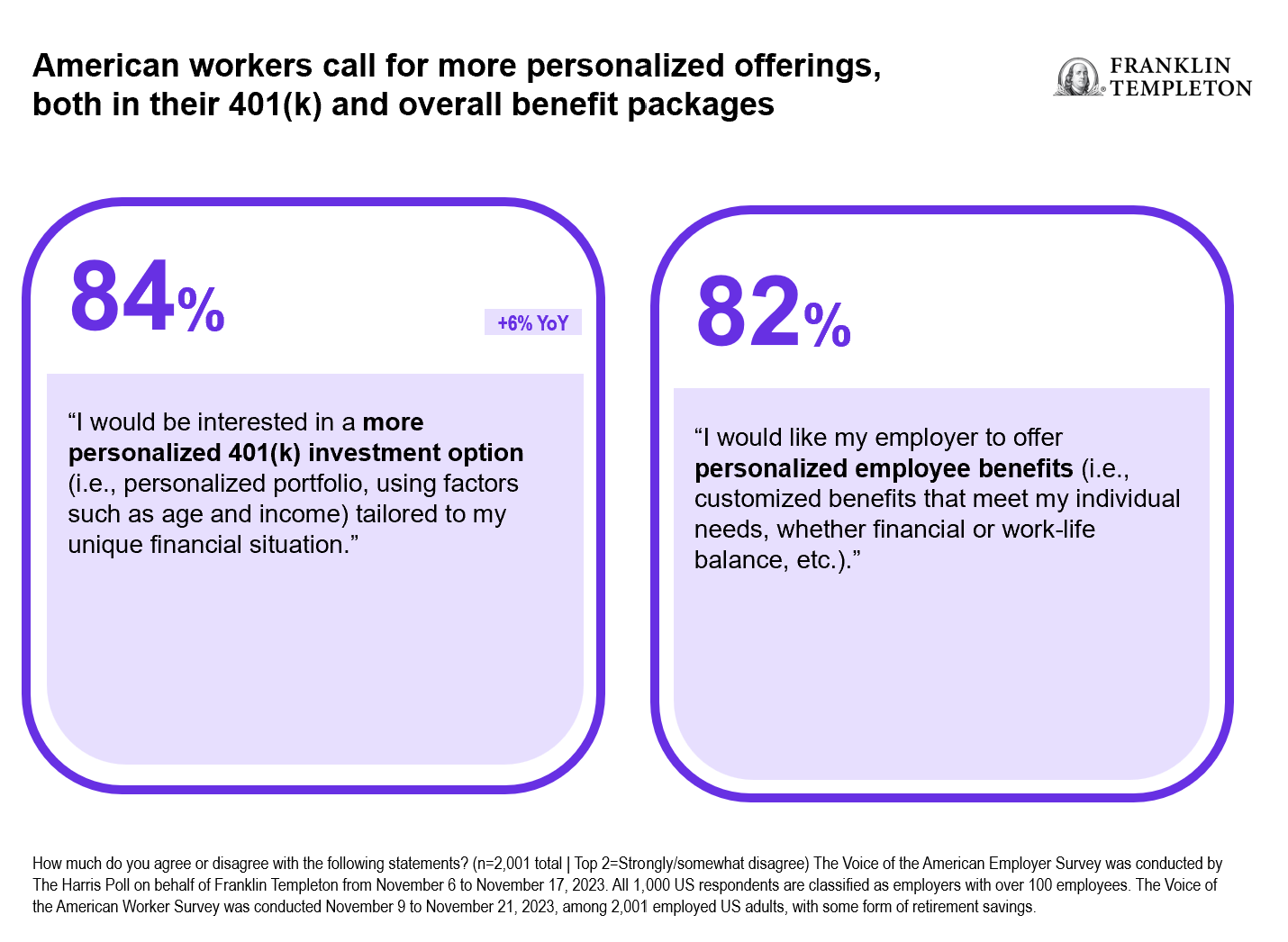

Customized plan design seeks to optimize participant outcomes and income replacement through tools like auto enrollment, auto escalation and stretch matches. Additionally, intentional engagement focuses on addressing holistic needs, including financial planning, budgeting, emergency savings and overall wellness.

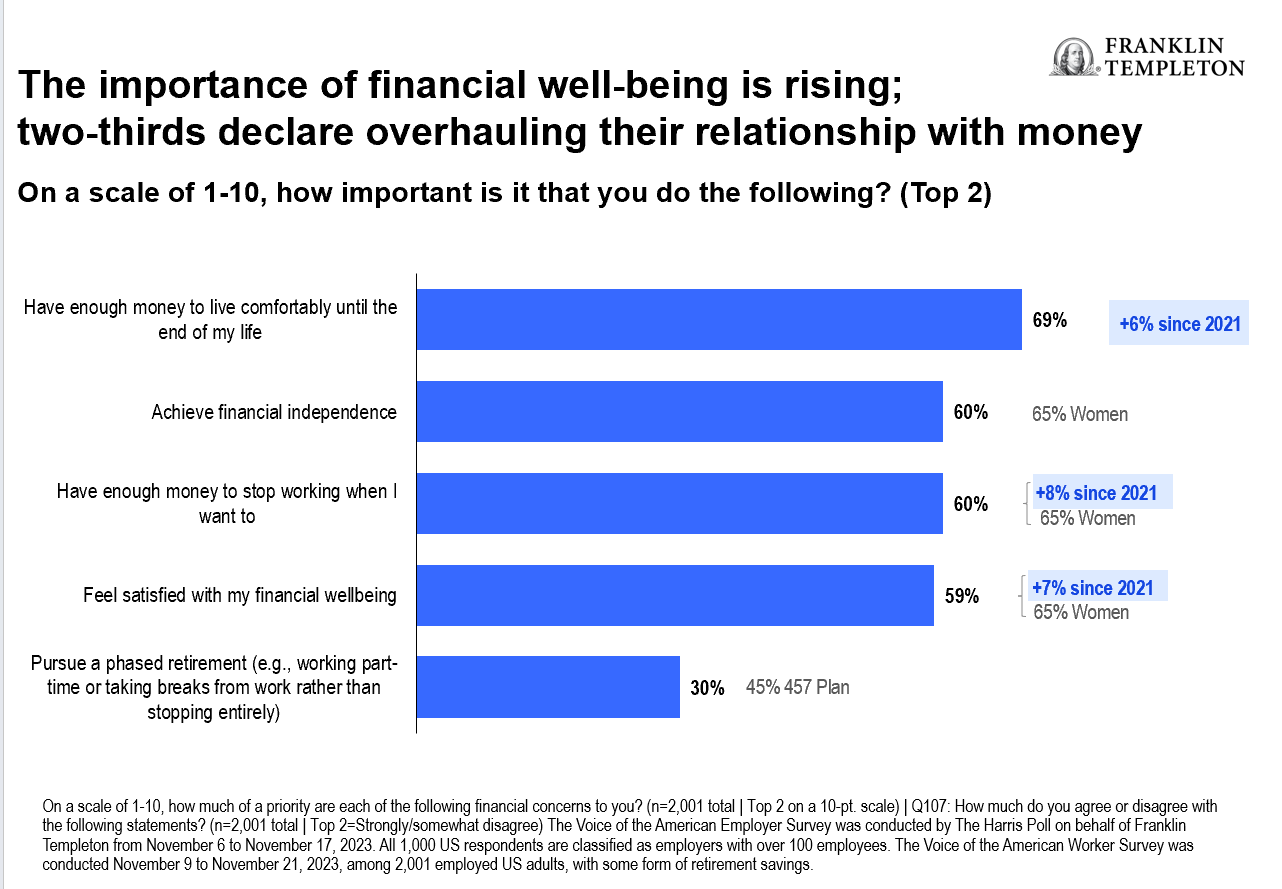

Employers and workers are already signaling change. We observe an example of the next normal in the participant’s view around saving and finance. Our 2024 Voice of the American Workplace Survey indicates the importance of financial wellbeing is rising among workers. Two-thirds of workers surveyed (65%) said they have overhauled their relationship with money.

(Right click on chart to enlarge/open in new window)

With the convergence of state mandates to offer workplace savings plans and SECURE Act provisions that cover many fees associated with new plan establishment, interest in workplace savings plans is growing. At the same time, there is a heightened focus on customization and employee engagement. New plans can be well designed from the start, while existing plans may benefit from a thoughtful redesign.

(Right click on chart to enlarge/open in new window)

As demands increase for customization, so does the adoption of automatic features. Features like auto enrollment and auto escalation take advantage of a principle James Clear wrote about in his book Atomic Habits. The “automatically in unless you opt out” nature of these design features makes it “require more work to get out of the good habit than to get started on it.”1

Turn insights into action

Here are three steps for retirement plan advisors to consider:

1. Learn Request For Proposal (RFP) systems: Become familiar with electronic proposal systems that seek to streamline and facilitate the RFP process.

2. Maximize practice efficiency: Investigate what role structured solutions—plans that have preselected fiduciary services and line ups—may play in maximizing the efficiency of your practice.

3. Optimize your client’s plan: Conduct plan reviews to ensure design innovation is providing a benefit for your existing clients as well as for new plans being formed. In other words, it seems prudent to put all existing plans through a review to determine whether the plan design is optimized.

As you consider the steps above, power your practice through partnership. Ask yourself, which partners actively work to make your practice more efficient? Which partners are your first call when you want to enhance what is working or overcome challenges?

Our retirement sales team is dedicated to walking with you to our next normal and the one after that. If thoughts like, “Change Has Never Been This Fast. It Will Never Be This Slow Again”2 are intimidating, recognize you have partners to help guide you. In particular, our Business Development Directors’ mission is to be your first call as you work on the initiatives outlined in this article.

For additional information, please contact the Franklin Templeton Retirement Sales Department at (800) 530-2432.

The Voice of the American Employer Survey was conducted by The Harris Poll on behalf of Franklin Templeton from November 6th to November 17th, 2023. All 1,000 respondents, based in the United States, are classified as employers, defined as having at least some influence over company benefits and/or hiring at organizations with over 100 employees. Respondents represent a mix of industries, company size, role, age, and race.

This presentation also references a qualitative study conducted by The Harris Poll on behalf of Franklin Templeton from August 15th to August 25th, 2023, among 15 American employers. All interviewees were full-time employees working in human resources, who have influence over employee benefits, and included those with titles such as HR Manager, HR Director or HR Vice President, among others.

This was a blind study, as Franklin Templeton was not mentioned in order to avoid bias.

The Voice of the American Worker Survey was conducted by The Harris Poll on behalf of Franklin Templeton from November 9th to November 21st, 2023, among 2,001 employed US adults. All respondents had some form of retirement savings. This online survey is not based on a probability sample and therefore no estimate of theoretical sampling error can be calculated.

Findings from 2020 reference a study of a similar nature that was conducted by The Harris Poll on behalf of Franklin Templeton from October 16 to 28, 2020, among 1,007 employed US adults, study from 2021 also references a similar survey conducted among 1,005 employed adults from October 28th to November 15th, and a study from 2022 also references a similar survey conducted among 1,000 employed adults from October 17th to October 27th.

Franklin Templeton is not affiliated with The Harris Poll, Harris Insights & Analytics, a Stagwell LLC Company.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Copyright © 2024 Franklin Templeton. All rights reserved.

______________________________________________________

1. Source: James Clear. Atomic Habits. Chapter 14. 2018.

2. Change Has Never Been This Fast. It Will Never Be This Slow Again (forbes.com), December 31, 2019.