With the threat of higher taxes on the horizon taxpayers are increasingly looking for ways to hedge that risk in retirement. This is especially true for those who have participated in an employer-sponsored retirement plan at their workplace for many years or even decades.

For many savers most, if not all, of their retirement savings are held within traditional, pretax accounts. Roth contributions within employer plans became available in 2006. But it has taken years for plans to add this feature and for participants to begin utilizing it as an option for a portion of their salary deferrals.

Of the $40 trillion retirement assets (ICI, Sept 2024), Roth accounts reflect a relatively low percentage of the overall total.

So, how can those who are still working and participating in an employer plan save more in Roth accounts without negative tax consequences on their current tax bill?

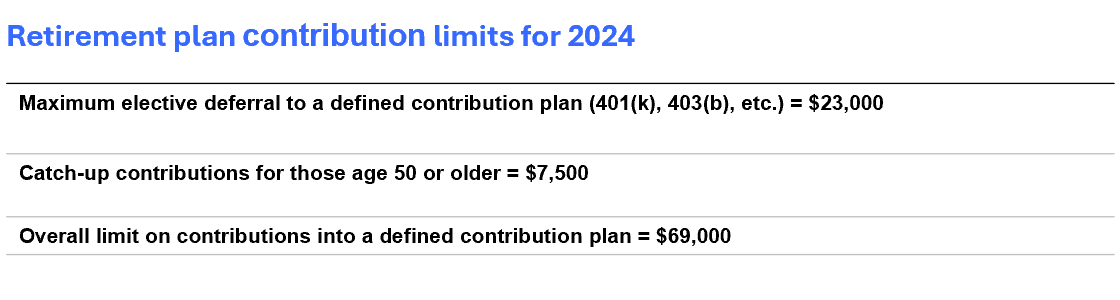

One strategy is to determine if your defined contribution plan allows voluntary, after-tax contributions into the plan. These are different from Roth 401(k) contributions made through salary deferrals. Voluntary after-tax contributions can be made in excess of your maximum salary deferral into the plan ($23,000 for 2024 not including catch-up contributions for those age 50 or older).

A benefit of making after-tax contributions within the plan (in excess your maximum salary deferral) is that these contributions, depending on specific plan guidelines, may be transferred to a Roth account within the plan, or directly transferred out of the plan to a Roth IRA. Since these are after-tax contributions, there is no tax when moving them from the after-tax portion to a Roth account. This action is sometimes referred to as a “mega backdoor Roth strategy.” It may be effective for higher earners who are maxing out their 401(k) plan to significantly fund a Roth account, even though their income restricts them from directly funding a Roth IRA. For 2024, income phaseouts on Roth contributions apply once modified adjusted gross income exceeds $146,000 for single filers and $230,000 for married couples filing a joint return.

Consider this example:

- Joan has participated in her 401(k) plan for many years making traditional, pretax contributions while also receiving employer matching contributions, also made pretax. While she is pleased with the sizeable savings within her plan, she is concerned about the impact of taxes when she begins distributions in retirement.

- This year, she is contributing the maximum amount of $23,000 (not including the catch-up contribution) into the plan through salary deferral. Because she is in a relatively high tax bracket, she is making pretax contributions.

- She receives a total employer contribution (match + profit sharing) of $16,000.

- The total of her own salary deferrals plus employer contributions totals $39,000.

- If her plan allows, Joan could contribute an additional $30,000 in after-tax dollars into the plan (up to the annual limit for all plan contributions of $69,000 for 2024).

- Pursuant to plan rules, Joan could transfer those after-tax contributions to either a Roth account within the plan, or a Roth IRA outside of the plan (participants must refer to the plan document for more details on options available to them).

In this example, Joan has effectively made a higher contribution to a Roth account $30,000) than is allowed within an IRA ($7,000 limit for 2024) without being restricted by her higher income level, which would not allow a Roth IRA contribution in her case.

Tax planning in retirement

For those who are “overweight” traditional, pre-tax retirement assets, this type of strategy can help to create some diversification by tax status. When drawing income in retirement, this may allow for more choice on where to draw funds from depending on the current tax environment, and personal tax circumstances. For example, if facing a lower tax bracket in a certain year, it may be advisable to withdraw more funds from a traditional retirement account to take advantage of lower tax rates. Conversely, if a higher tax bracket applies, it may be more advisable to withdraw from a Roth account if additional income is needed. It’s important to note that many retirement plans do not offer the option of making voluntary, after-tax contributions into the plan. Depending on the plan’s characteristics, these types of extra after-tax contributions can lead to issues with discrimination tests required of ERISA plans if a high proportion of highly-compensated employees are taking advantage of this feature.

Seek professional advice

Since individual circumstances will vary widely, it’s important to work with an advisor knowledgeable of managing income and taxes in retirement, who is also aware of your personal financial situation and objectives. For those who require modest income in retirement and expect to be in a low tax bracket, holding funds in a Roth account may not make sense. But for many, having a mix of traditional, pretax retirement funds and Roth savings can provide more flexibility to manage taxes in retirement.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as, investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon, by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.