- The shift from a zero-interest rate environment to one with higher yields and inflation uncertainty makes capital preservation choices more significant for long-term retirement outcomes.

- Stable value funds are essential for retirement plans as they can potentially provide the two outcomes plan participants seek for capital preservation: the price stability of cash with inflation-beating returns.

- As stewards of their employees’ retirement savings, we suggest plan sponsors revisit their capital preservation options to make sure they deliver the outcomes their plan participants need to fulfill their retirement objectives.

Plan sponsors have much to consider when designing and maintaining a workplace retirement plan. Employee demographics, plan design, and selecting investment managers are just a few of the key factors.

One step of the decision-making process might seem less complicated—selecting a capital preservation option for the plan. This task may initially seem less difficult than choosing an investment in the target-date, equity or fixed income categories because the objective of capital preservation appears more straightforward than higher-return, higher-risk asset classes.

However, plan sponsors need to be aware of the varied approaches to capital preservation and prioritize the careful evaluation of the landscape of investment options and the underlying risk/return that comes with them.

The environment for capital preservation has fundamentally changed

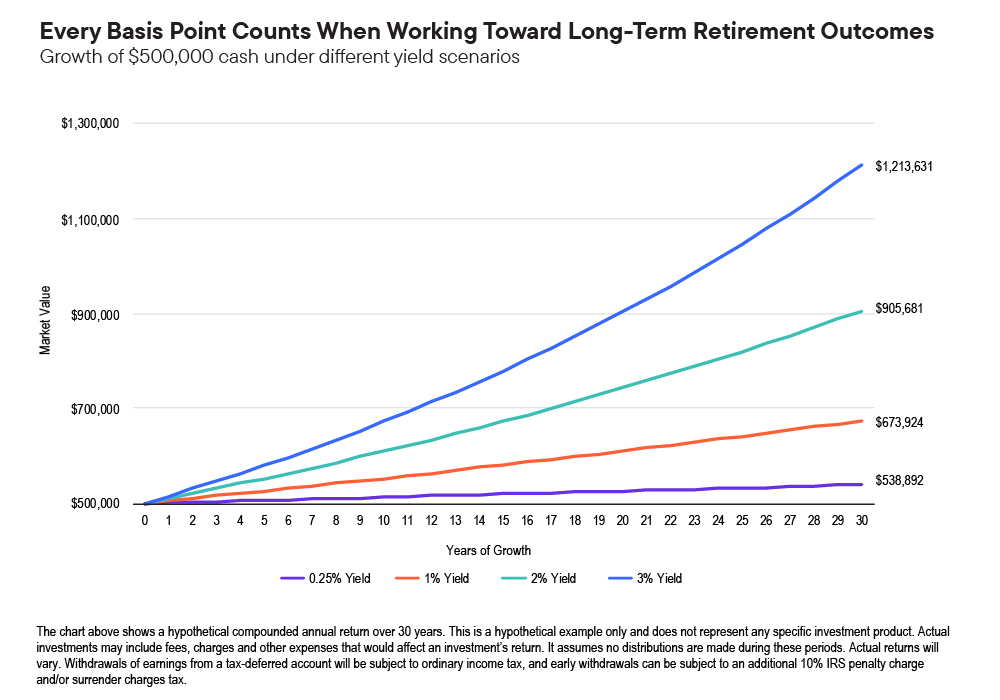

Today’s higher interest rate environment makes retirement plan cash management decisions even more crucial than during the past decade. When the Federal Reserve (Fed) finishes its rate cutting cycle, short-term interest rates are likely to settle in the range of 3%-4%, a level that can materially affect participants’ accumulation and income over a long horizon.

The figure below illustrates that when cash yields averaged 0.25%, which was the case for nearly 15 years—the accumulation differences were marginal over a 30-year time horizon. But if yields revert closer to their long-term average of around 3%, accumulation differences can determine whether a plan participant has either a cash-strapped or a comfortable retirement.

With interest rates normalizing, capital preservation options are offering competitive, inflation-beating return potential. Combined with low volatility, these strategies may be essential to help plan participants reach retirement goals.

In addition to the re-setting of interest rates, the inflation landscape has also changed. Inflation is top of mind for most savers, and there will likely be more inflationary than disinflationary shocks in the foreseeable future. This shift in sentiment may have profound implications. With inflation still running above long-term averages, maximizing yield while balancing returns with capital preservation is essential to building and protecting the real value of participant savings.

The environment for capital preservation will change again

Stable value funds typically invest in high-quality, short- to intermediate-term bonds, with an average duration of 2–4 years. Because stable value funds invest in longer maturity bonds from a more diverse set of opportunities, they typically outperform money market funds and the rate of inflation.

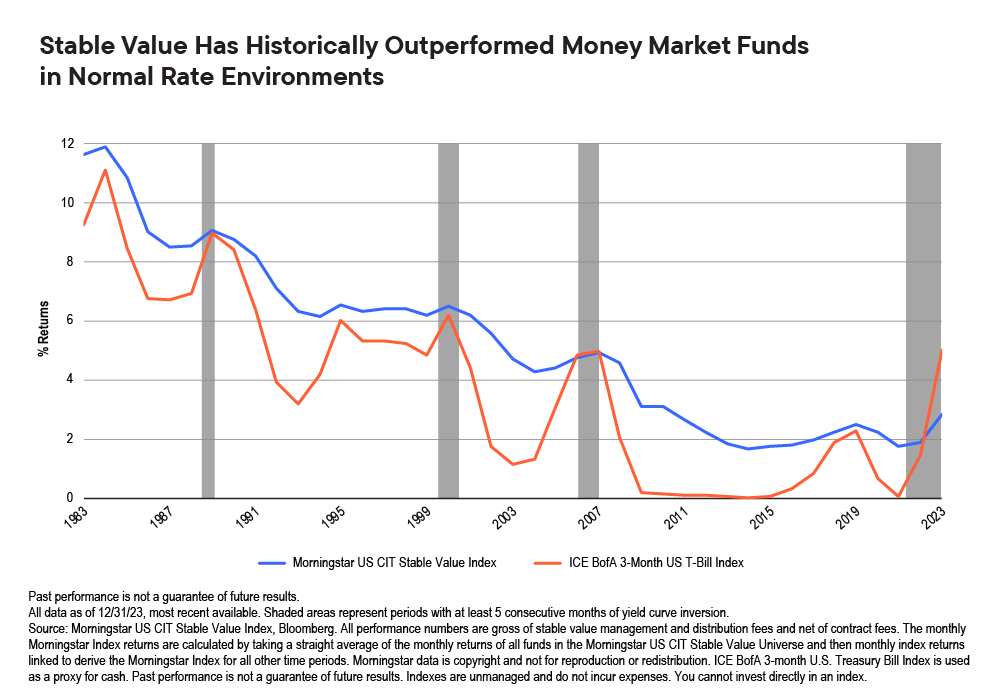

Many retirement plans use government money market funds which are required to invest in very high-quality assets like short-term government securities, such as treasuries, agencies and repurchase agreements. Money market funds are very short-term in nature, so their yields tend to closely follow the Federal Funds rate. (In the following chart, the 3-month US T-Bill Index is used as a proxy for cash or money market funds.)

Through most of the last 15 years, stable value funds offered a considerable return premium over money market funds within retirement plans. However, the market environment was turned on its head when the Fed embarked on its aggressive tightening cycle in early 2022.

Short-term interest rates climbed rapidly, inverting the yield curve, and money market rates reacted very quickly, surpassing stable value yields for the first time in over 15 years. This was expected because stable value funds have a longer duration, meaning their portfolios do not turn over nearly as quickly as money market funds.

The inverted yield curve has had a significant impact on all financial markets, including capital preservation. In most market environments, stable value funds have outperformed money market funds on an annual basis—in fact, this current period is an anomaly when you compare the history of both investment options going back 40+ years.

Looking ahead, as the Fed further normalizes rates, we expect this dynamic to once again shift towards a more typical environment where long-term yields are higher than short-term yields. As a result, stable value funds will regain the return advantage they have historically enjoyed over money market funds.

Why stable value is built for the long term

Stable value funds possess unique structural advantages that make them well-suited to deliver what plan participants need in a capital preservation option: price stability, inflation-beating returns, and a smoother return experience that provides a sense of confidence.

Advantage 1: Book value accounting results in price stability

Stable value funds benefit from a specific accounting standard that allows market value assets to be valued at book value rather than using daily mark-to-market accounting. As a result, the fund’s net asset value (NAV) remains constant, hence the name stable value.

In contrast, short and intermediate-term bond mutual funds have a floating NAV, making investments in them much more volatile. Crucially, stable value vehicles purchase insurance contracts, also known as “wraps” and/or guaranteed investment contracts (GICs), to protect participant balances from daily price volatility and allow for qualified transfer and withdrawal activity at a $1 NAV, just like money market funds.

Advantage 2: Longer duration results in inflation-beating returns

Stable value funds have historically provided higher returns relative to money market funds and competitive returns compared to intermediate-term bonds. Stable value funds characteristically invest in high-quality, short- to intermediate-term bonds, with a typical fund’s average duration between two to four years.

The longer duration helps lift returns above those of money market instruments and is comparable to more volatile intermediate bond strategies. With longer duration comes incremental risk, which investors are rightfully compensated for over the long term and is of less concern given the insurance protection provided by the wrap and GIC issuers. This boosts the accumulation advantage of stable value funds.

Advantage 3: Crediting rate results in a smoother ride for participants

Crediting rates are a unique return mechanism used in stable value funds. Crediting rates can be thought of as a similar metric to the “yield” of a traditional fixed income portfolio.

Unlike a traditional bond portfolio, where market value fluctuations impact the net asset value and

ultimately the participant’s principal balance, price changes in the underlying portfolio of a stable value fund are experienced through the crediting rate. Specifically, the crediting rate adjusts for any market value gains or losses from the underlying bond portfolio(s). Ultimately, the long-term goal is the convergence of the underlying market value with the book value owed to participants.

As a result of this mechanism, the crediting rate “smooths” the return stream of a stable value fund which insulates investors from short-term principal fluctuations due to changes in the market value of individual underlying securities.

A range of choices to consider

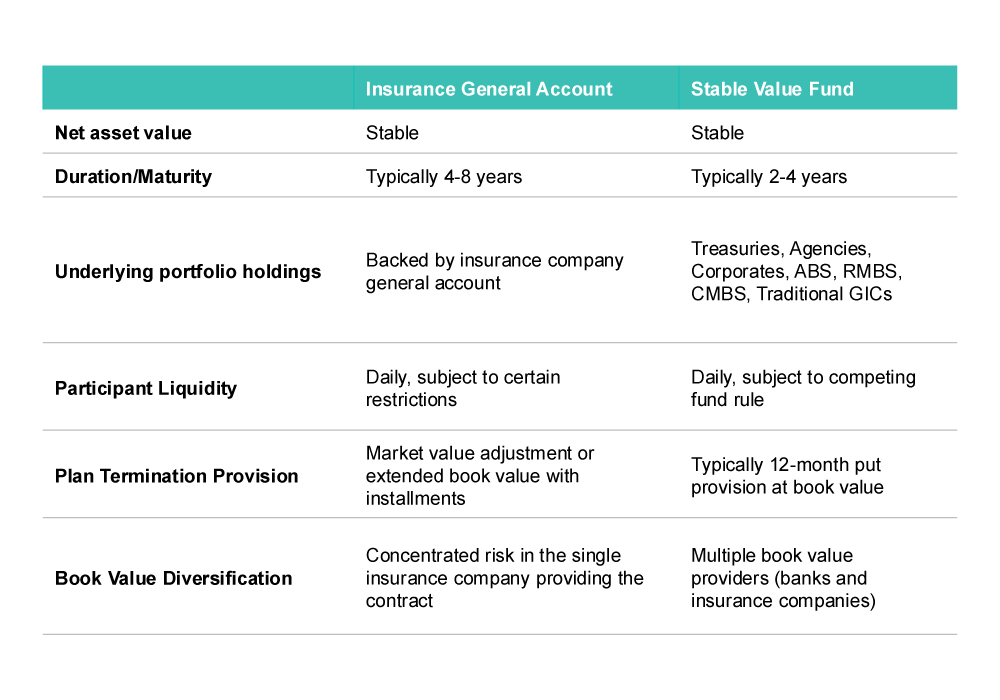

The stable value category includes different types of vehicles. Third-party stable value funds are typically structured as a collective investment trust (CIT) or as a segregated account for a specific plan or trust. Additionally, there are stable value products directly issued by insurance companies. These include products backed by the issuing insurance company’s general account assets or vehicles that are backed by a segregated asset account.

When evaluating a stable value option, there are several key questions to consider:

- Vehicle type: CIT or insurance product

- Management team track record

- Product structure and philosophy: Does the manager favor total return or liquidity

- Diversification of underlying investments

- Diversification of book value providers: Single or multiple “wrap” providers

- Participant and plan level liquidity (exit) provisions

- Transparency of underlying portfolio

While capital preservation comparison tools are not as prevalent as tools for other asset classes, contact your Franklin Templeton Retirement Plan Specialist to request an analysis of the capital preservation funds you currently use.

WHAT ARE THE RISKS?

All investments involve risk, including loss of principle.

Stable value funds seek capital preservation, but there can be no assurances that they will achieve this goal. Stable value funds’ returns will fluctuate with interest rates and market conditions. The funds are not insured or guaranteed by any governmental agency. Funds that invest in bonds are subject to certain risks including interest-rate risk, credit risk, and inflation risk. As interest rates rise, the prices of bonds fall. Long-term bonds are more exposed to interest-rate risk than short-term bonds. Unlike bonds, bond funds have ongoing fees and expenses.

Government money market funds typically invest at least 99.5% of the fund’s total assets in cash, US government securities and repurchase agreements. You could lose money by investing in the fund. Although the fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. An investment in the fund is not a bank account and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Interest rate increases can cause the price of a money market security to decrease. A decline in the credit quality of an issuer or a provider of credit support or a maturity-shortening structure for a security can cause the price of a money market security to decrease.

Retail money market funds: You could lose money by investing in the fund. Although the fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. An investment in the fund is not a bank account and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The fund’s sponsor is not required to reimburse the fund for losses, and you should not expect that the sponsor will provide financial support to the fund at any time, including during periods of market stress.

Past performance is no guarantee of future results.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as, investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliates, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon, by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax professional.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Copyright © 2025 Franklin Templeton. All rights reserved.

Ref. 4447558