Wealth managers have historically struggled on how best to support clients that own small businesses. However, current regulation and enhancements in retirement plan structures make offering 401(k) plans to small businesses much easier and less expensive.

This is a win-win-win situation. It’s a win for our broker-dealer and advisor partners seeking to add “stickier assets” to their book of business by offering retirement plan services to their clients. It’s a win for the business owner as tax credits are now available to help mitigate the costs of a retirement plan. And it’s a win for the employees of the business that want an attractive retirement savings option.

Let’s dive into the tax deal that awaits small businesses…

Small business owners who do not currently offer a workplace retirement plan, now have an attractive tax deal to start one. By small, I mean businesses with 50 or fewer employees. Section 102 of the SECURE Act 2.0 of 2022 (SECURE 2.0) enhances and expands the tax credits available for your business if you establish a new simplified employee pension (SEP), savings incentive match plan for employees of small employers (SIMPLE) plans or qualified retirement plan like a 401(k) plan.

First, for businesses with up to 50 employees without a retirement plan that establish a SEP, SIMPLE IRA or 401(k) plan, Section 102 of SECURE 2.0 increases the small plan startup tax credit from 50% to 100% of eligible costs (capped at $5,000 per year) for the first three years the plan exists. (Prior rules still apply for those with 51-100 employees.)

More precisely, the enhanced credit is 100% of the eligible startup costs, up to the greater of:

$500; or

The lesser of

- $250 multiplied by the number of non-highly compensated employees (non-HCEs) who are eligible to participate in the plan, or

- $5,000.

Other eligibility rules include:

- The business had at least one plan participant who was a non-HCE; and

- In the three tax years before the first year the business is eligible for the credit, the covered employees were not substantially the same employees who received contributions or accrued benefits in another plan sponsored by the business.

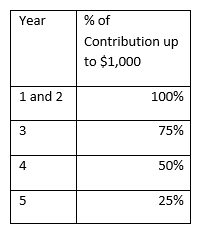

Second, the new law also added an additional credit exclusively for defined contribution plans with 50 or fewer employees. The credit is equal to a percentage of the amount an employer contributes on behalf of employees, up to a per-employee cap of $1,000. Employees with compensation in excess of $100,000 are excluded from the calculation. This credit applies for five years and is phased out for employers with between 51 and 100 employees.

But don’t forget about the third potential plan startup credit that exists under the old rules, which are still applicable. An eligible employer that adds an auto-enrollment feature to its plan can claim a tax credit of $500 per year for a three-year period beginning with the first taxable year the employer includes an auto-enrollment feature.

Let’s talk numbers with an example. Consider the following scenario.

- In 2023, Biz Inc., sets up a new auto-enroll 401(k) plan with a 100% match up to 4% of compensation.

- The company has 19 employees: 17 are non-HCEs and two are HCEs.

- There are eight employees with compensation over $100,000 and there are 11 employees each with compensation of between $25,000-$100,000.

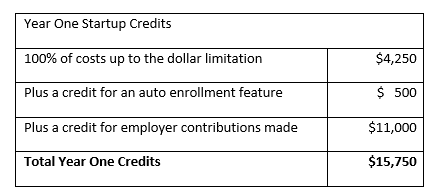

- Biz Inc.’s, total startup costs for year one = $7,500

Credit #1 Startup Credit

Biz Inc.’s credit is subject to a dollar limitation, which is the greater of $500 OR the lesser of A or B.

- $4,250 (i.e., $250 x 17 non-HCE participants)*

- $5,000

Result= $4,250

*20-50 non-HCEs would impose the $5,000 yearly cap

Credit #2 Auto Enrollment

Credit for auto enrollment feature = $ 500

Credit #3 Employer Contributions

11 employees with comp < $100K x $1,000= $11,000

Businesses will likely use an updated version of Form 8881, Credit for Small Employer Pension Plan Startup Costs and Auto-Enrollment to claim the credits.

What about businesses that will join or have joined multiple employer plans (MEPs) or Pooled Employer Plans (PEPs)? Fortunately, Section 111 of SECURE 2.0 ensures the startup tax credit is available for three years for employers joining a MEP or PEP, regardless of how long the MEP or PEP has been in existence.

The enhanced plan startup credit and credit for employer contributions for businesses with 50 or fewer employees is effective for the 2023 and later tax years. How do these changes impact plans started a year or two ago—are they simply out of luck? If a business established a plan within what we call “the establishment window” (i.e., three years to be eligible for the startup and auto enroll credit, and five years to be eligible for the employer contribution credit), and it meets the other eligibility criteria mentioned earlier, it would be eligible to claim the credits for the years remaining in the establishment window.

Returning to our prior scenario, let’s say that Biz Inc., had set up its plan in 2021. Biz Inc. would be able to claim the enhanced startup tax credit for one year—2023, and the new employer contribution credit for 2023-2025. If Biz Inc. was an eligible employer in 2021 under the startup credit rules in effect prior to the SECURE 2.0 Act changes, it would have applied 50% (rather than 100%) when calculating the maximum credit amount for 2021 and 2022. Biz Inc. would also have been able to claim the $500 auto-enroll credit for 2021 and 2022.

An enticing tax deal may await small businesses that do not currently offer workplace retirement plans. SECURE 2.0 enhances current plan startup tax credit rules and adds a new tax credit for employer-provided contributions. Plus, the $500 spiff for adding an auto-enroll feature may apply as a result of the prior rules that are still applicable.

Contributions provided by the Retirement Learning Center, LLC, a third-party industry consultant.

IMPORANT LEGAL INFORMATION

Franklin Templeton (FT) does not provide legal or tax advice. The information provided in this document is general in nature, is provided for informational and educational purposes only, and should not be construed as investment, tax or legal advice, or as an investment recommendation within the meaning of federal, state, or local law. Laws and regulations are complex and subject to change. Statements of fact come from sources considered reliable, but no representation or warranty is made as to their accuracy, completeness or timeliness. FT makes no warranties with regard to information in this document or results obtained by its use, and disclaims any liability arising out of the use of, or any tax position taken in reliance on, such information.

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the author and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this presentation has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Franklin Distributors, LLC. Member FINRA/SIPC. Prior to July 7, 2021, Franklin Templeton Distributors, Inc., and Legg Mason Investor Services, LLC served as mutual fund distributors for Franklin Templeton.