As the new administration explores options to reduce federal government spending, concerns are rising around changes to Social Security. For example, what actions may be considered that could potentially impact Social Security benefits? While there have been discussions around closing offices or reducing the workforce of the Social Security Administration, making structural modifications to Social Security, such as raising the retirement age, are more complicated. For this reason, major changes to Social Security in the near term are unlikely.

Republican lawmakers are currently pursuing tax and spending-related changes through a process known as budget reconciliation. To gain more understanding of the reconciliation, see our recent post, “Tax policy takes center stage: What to watch on Capitol Hill.” This process allows lawmakers to pass legislation in the Senate with a simple majority, avoiding the 60 vote-threshold needed to avoid a filibuster. Even with slim majorities in both chambers of Congress, the Republicans can advance a bill without Democrat votes.

However, Senate procedural rules prevent using the budget reconciliation process to make changes to Social Security. The Congressional Budget Act of 1974, which introduced budget reconciliation, explicitly prevents changes to Social Security unless normal rules are followed. Since it’s probably unlikely that we’ll see a party control at least 60 seats in the Senate, making major changes will require bipartisan support. Latest projections call for the Social Security Trust Fund to be depleted in 2035, causing a roughly 20% reduction in benefits, unless Congress takes action.

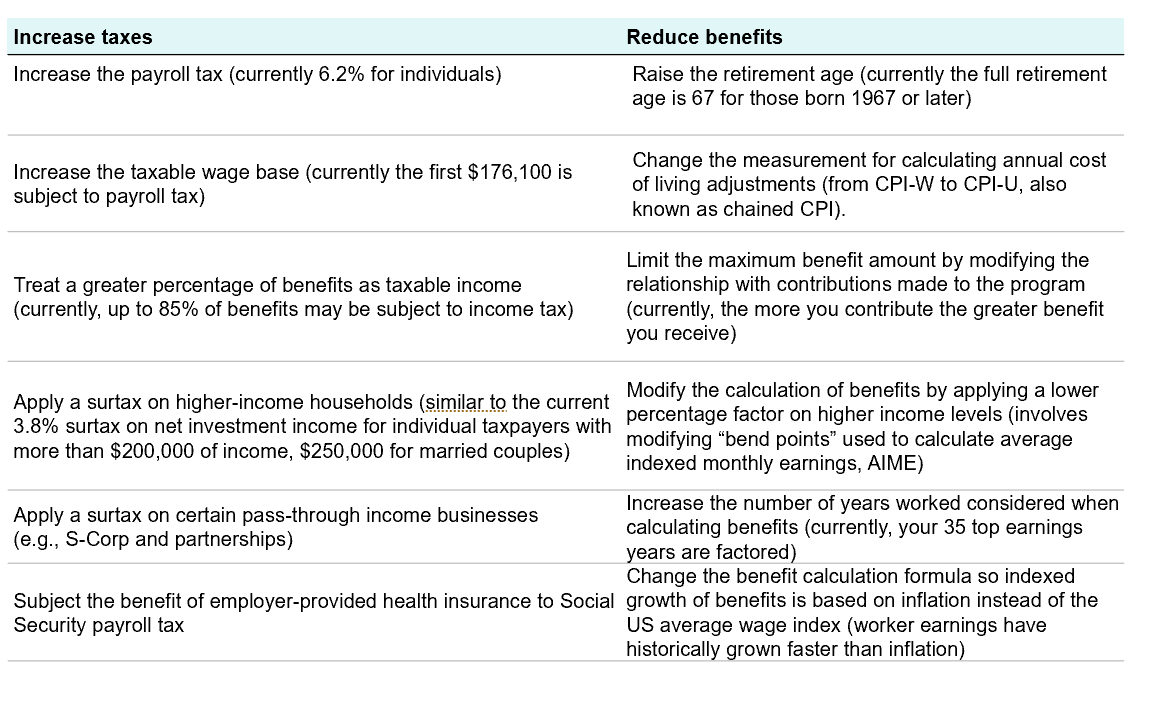

Here are some potential policy options to fix Social Security:

Additional points to address the challenge

- Currently, employment earnings below $176,100 are subject to the Social Security payroll tax. Some lawmakers have proposed increasing that threshold, exposing more earnings to payroll tax. One plan would maintain that threshold but also apply payroll taxes on earnings over $250,000. That would mean, based on current limits, a worker’s first $176,100 would be subject to the 6.2% payroll tax and then the payroll tax would apply again on all earnings above $250,000. This would result in a “donut hole” where earnings between $176,100 and $250,000 would not be subject to Social Security payroll tax. Making this adjustment would result in generating significant revenue.

- Originally, the taxable wage base was designed to cover 90% of earnings in the United States. Currently, 83% of earnings are subject to Social Security payroll tax since wages for higher-income taxpayers have grown faster than those of lower-income taxpayers. If policymakers wanted to reach the 90% target now, the taxable wage base would have to increase to roughly $300,000.

- Some proposals call for including all state and local employees as part of the Social Security system. In some states and municipalities, employees are covered by a separate retirement program instead of Social Security (roughly 5% of workers nationwide are not covered by Social Security).

Considerations for retirement planning

The long-term future of Social Security is in the balance. However, even if Congress doesn’t act, beneficiaries are projected to receive roughly 80% of scheduled benefits. There is confusion that the depletion of the trust fund will mean that benefits are completely gone. This is not the case. However, prudent planning must incorporate the risks of a reduced benefit amount in the future, higher taxes, or both.

- Younger investors should factor in potential benefit reductions in Social Security as part of a comprehensive retirement savings and income plan. Look for opportunities to increase savings as early as possible.

- Take a thoughtful approach to claiming Social Security, especially if those benefits are the only source of guaranteed, lifetime income. Avoid making a rash decision to claim Social Security early just because you’ve heard that the trust fund is being exhausted. An eventual plan to address the issue will likely not impact current and near retirees as much as younger workers.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon, by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Copyright © 2025 Franklin Templeton. All rights reserved.

Endnote

______________________________

Sources: 2024 Social Security Trustees Report, American Academy of Actuaries.

Ref. 4252909