US Federal Reserve (Fed) Chairman Jerome Powell hedged himself very carefully in the press conference following the July 27 Federal Open Market Committee (FOMC) meeting. Financial markets heard only what they wanted to hear and ignored the rest. Markets chose to hear that the “Fed put” is alive and well, and it fueled a rally in both equities and bond yields. I think this just sets the stage for a correction, and more volatility ahead.

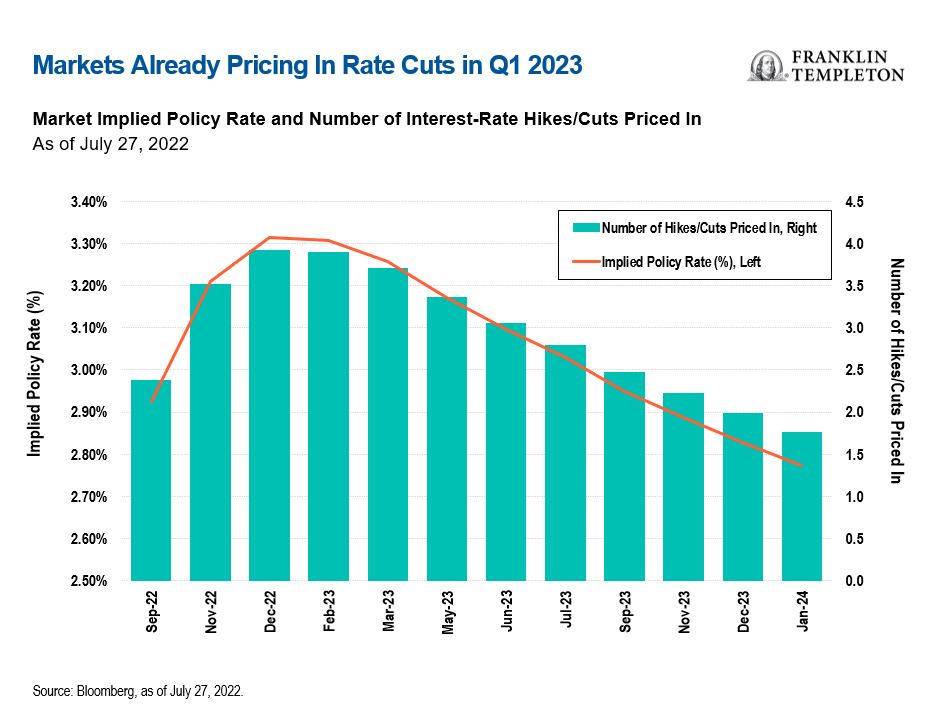

Powell said that policy interest rates are now in the neutral range (I disagree, but more on this later), the economy has started to weaken, and that the full impact of the rate hikes delivered so far has yet to be felt. This reinforced the markets’ conviction that we are approaching the peak of the tightening cycle, and that by the first quarter (Q1) of next year, the Fed will reverse course and start cutting rates. Indeed, markets now expect 50 basis points (bps) of rate cuts next year.

But Powell also said that the FOMC’s June views on the likely path of rates still stand, and those views suggest the Fed would keep hiking into 2023 to a peak of about 3.8%. Powell noted that another “unusually large” rate hike in September could not be ruled out. He underscored the persistent strength of the labor market and said that bringing inflation back to target will require slower growth and higher unemployment. So far, markets do not seem to have paid much attention to that part.

Commenting on the June press conference, I had noted that the Fed had de facto abandoned forward guidance; today, nearly all commentators agreed that forward guidance is gone, as Powell was even more emphatic in stressing that uncertainty is high, the Fed has very little visibility and will choose its next moves meeting-by-meeting as new data come in.

I think Powell could have been more forceful in indicating that, with inflation at 40-year highs and unemployment at 50-year lows, the Fed has a ways to go to bring demand and supply back in balance and restore price stability. But—as he admitted—the Fed’s previous forecasts of how quickly inflation would fade have proved totally wrong, so we can’t fault him for taking a humbler and more data-dependent stance.

This, however, makes the Fed’s job more complicated to the extent that the rally in equities and the decline in bond yields drive a meaningful easing in financial conditions, undoing part of the Fed’s work. Moreover, I continue to disagree with the Fed on the neutral interest rate: I don’t think the neutral range is as low as 2.0%–2.5% in nominal terms—and by the way, we’re talking about the rate that would be neither restrictive nor expansionary with US inflation at 2%, not with inflation at the current 9%. Meanwhile, the labor market remains hot and activity fairly resilient, partly thanks to robust household balance sheets.

Overall, while we might get some help from lower gas prices in the next print, I think underlying inflation will remain stubbornly high for the remainder of the year. Importantly, higher than markets think and the Fed hopes. This, in turn, should compel the Fed to keep hiking into next year. I think the terminal rate will be much closer to having a “4” handle; but even if the Fed stops below that, I believe it will have to keep rates at their chosen plateau through a large part of next year to convincingly rein in inflation. The idea that a steep easing cycle could start as early as Q1 2023 seems far-fetched, in my view.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.